Date Issued – 25th November 2024

Preview

Howard Lutnick, Trump’s Commerce Secretary nominee, is in talks with Tether for a $2 billion bitcoin lending project that could scale to tens of billions. China’s dairy boom is slowing, with revenue for top producers dropping up to 13% in H1 2024 amid overcapacity and demographic shifts. The U.S. bond market is stabilizing after Scott Bessent’s Treasury nomination, but volatility persists over fiscal policy uncertainty. Meituan and Chow Tai Fook’s earnings will gauge China’s struggling consumer market. ElectraLith, a Rio Tinto-backed lithium startup, nears a $19 million fundraise for its innovative, cost-efficient extraction technology despite weak markets. Trump’s anticipated tariffs threaten Southeast Asia’s trade growth, potentially impacting semiconductors, EVs, and clean energy sectors.

Trump Nominee Lutnick in Talks with Tether for $2B Bitcoin Lending Push

Howard Lutnick, U.S. President-elect Donald Trump’s pick for Commerce Secretary, is reportedly eyeing a $2 billion bitcoin-backed

lending project in collaboration with Tether, the issuer of the largest stablecoin. Lutnick’s firm, Cantor Fitzgerald, is in discussions

to leverage Tether’s financial support for the initiative, which could scale to tens of billions of dollars. Tether, which already works

closely with Cantor to manage billions in U.S. Treasuries backing its stablecoin, confirmed its interest in exploring new investment

opportunities. This move underscores Lutnick’s advocacy for cryptocurrency adoption as he prepares to lead the Commerce Department.

Investment Insight: A partnership between a major financial firm and Tether signals growing institutional interest

in crypto-backed lending, but regulatory scrutiny and market volatility remain key risks for investors.

Trump’s Tariff Policies Threaten Southeast Asia’s Trade Growth

Donald Trump’s anticipated return to the White House raises concerns for Southeast Asian economies like Malaysia, Thailand, and Vietnam,

which previously benefited from his trade war with China. During Trump’s first term, Chinese firms relocated supply chains to the region,

boosting investment and jobs. However, the new administration’s focus on curbing “third-country workarounds” could result in tariffs as

high as 20% on imports from nations with large trade surpluses, particularly in strategic sectors like semiconductors and electric vehicles.

Steve Alain Lawrence, CIO of Balfour Capital, suggests that affected Asian nations could retaliate with tariffs on U.S. goods or impose

non-tariff barriers, further complicating trade dynamics. Analysts warn of potential export declines, retreating foreign investment, and

strained manufacturing supply chains, while regional governments explore free trade agreements and alliances to mitigate risks.

Investment Insight: Southeast Asia’s trade-reliant economies may face headwinds as Trump’s protectionist policies target

supply chain reconfigurations. Investors should monitor impacts on semiconductors, EVs, and clean energy sectors while considering

diversification into resilient industries and regions.

China’s Dairy Boom Nears Its End, S&P Warns

China’s decades-long dairy expansion is slowing, with revenue for the top three producers dropping up to 13% in the first half of 2024,

according to S&P Global Ratings. A shrinking population and sluggish economy are expected to halve annual growth in dairy sales volumes

to 2%-3% over the next 20 years. Overcapacity and a 40% rise in domestic milk production over the past decade have further exacerbated

pressure on the sector. While the government considers limiting EU imports to ease strain on farmers, S&P predicts the aging population

may stabilize demand in 10 to 15 years.

Investment Insight: China’s dairy industry faces structural challenges, including demographic shifts and overproduction.

Investors should anticipate volatile earnings and focus on companies adapting to long-term trends like aging-related consumption.

Bond Market Stabilizes as Bessent’s Treasury Nomination Calms Markets

The U.S. bond market is finding its footing after a two-month selloff, with investors stepping in at 4.5% yields.

Treasury yields, which peaked on Nov. 15, have since dipped to 4.36% following Scott Bessent’s nomination as U.S. Treasury Secretary.

Bessent, a fiscal hawk, has pledged to cut the deficit to 3% of GDP through spending cuts and economic growth, though skeptics question

the feasibility of reducing essential expenditures like Medicare and defense. His commitment to a strong dollar contrasts with Trump’s

past devaluation rhetoric, and his fiscally disciplined stance has eased market concerns, driving a 6-basis-point drop in 10-year yields.

Despite the recent rally, uncertainty over Trump’s fiscal policies, inflation, and potential tariffs—some as high as 60% on Chinese goods—keeps

volatility elevated. While some strategists see 4.25%-4.5% as fair value for 10-year Treasuries, others caution that yields could rise further

if aggressive fiscal stimulus boosts inflation. Traders are now awaiting the Fed’s preferred inflation gauge, the PCE price index, for additional clarity.

Investment Insight: Treasuries at 4.5% yields present attractive returns, but volatility may persist amid fiscal policy uncertainty.

Bessent’s nomination signals fiscal discipline, which could support bonds but pose risks for equities if aggressive deficit reduction slows growth.

Investors should monitor tariff developments, Fed-ECB rate divergence, and inflation data for guidance.

US10Y Yield: 4.328%

Meituan, Chow Tai Fook Earnings to Gauge China’s Consumer Sentiment

Earnings from Meituan and Chow Tai Fook Jewellery this week are set to provide insights into China’s struggling consumer market, weighed down

by a sluggish economic recovery, property woes, and job instability. Despite these headwinds, October retail sales saw their fastest growth in

eight months, supported by government stimulus efforts that have yet to meaningfully boost household incomes.

Meituan is expected to defy the broader slowdown, with Morgan Stanley predicting strong growth driven by consumption voucher programs and

policy support for platform economies. In contrast, Chow Tai Fook’s first-half earnings are likely to reflect weak retail sentiment and high gold prices,

with revenue projected to decline up to 22%.

Investment Insight: Meituan’s resilience highlights opportunities in platform-driven sectors benefiting from policy tailwinds,

while Chow Tai Fook underscores challenges in discretionary spending. Cautious positioning in China’s consumer sector is warranted until income growth stabilizes.

Market price: Meituan (3690.hk): HKD 161.00

Rio Tinto-Backed Lithium Startup Nears $19M Fundraising Amid Market Struggles

ElectraLith, a Rio Tinto-backed lithium technology startup, is set to close an oversubscribed A$29 million ($19 million) funding round despite weak global lithium

and venture capital markets. The company’s innovative direct lithium extraction (DLE) technology uses no water or chemicals, making it ideal for arid regions like

Chile’s Atacama Desert. ElectraLith plans to use the funds to construct its first pilot plant at Rio Tinto’s Rincon operations in Argentina within a year, followed

by two additional pilot plants. The DLE-R process, which filters brine to produce lithium hydroxide at half the cost of competitors, could revolutionize the lithium

industry by drastically shortening production timelines and addressing water scarcity challenges.

Investment Insight: ElectraLith’s cost-efficient and sustainable DLE technology positions it favorably in the growing lithium market,

which could surpass $10 billion annually within a decade. Investors should watch how the startup scales its technology and competes in the evolving EV battery supply chain.

Market Price: Rio Tinto: USD 62.50

Conclusion:

The global investment landscape is rapidly evolving, shaped by geopolitical shifts, technological innovation, and changing consumer trends.

As the U.S. navigates a political transition and China faces structural challenges, Southeast Asia grapples with the potential fallout from

Trump’s protectionist policies. Investors must remain vigilant, monitoring developments in key sectors like cryptocurrencies, bonds, consumer

goods, lithium, semiconductors, and EVs. Diversification and adaptability will be crucial in mitigating risks and seizing opportunities amidst

uncertainty. The coming weeks will provide further clarity on the future of these critical industries and the economies they support, as the world

braces for a new era of change.

Upcoming Dates to Watch:

November 28, 2024: Eurozone Economic Sentiment Indicator release

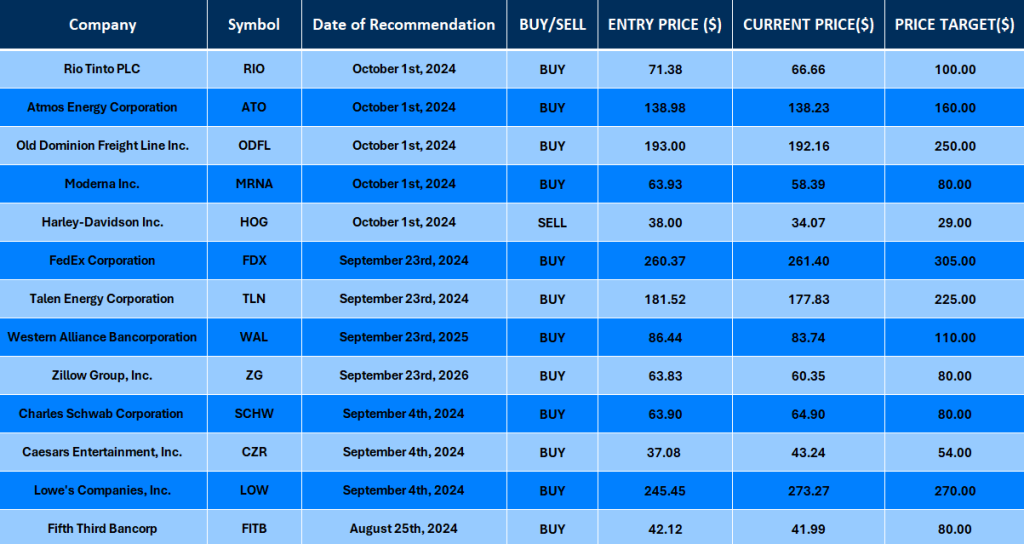

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.