Date Issued – 4th November 2024

Preview

Today’s newsletter covers impactful developments across labor, automotive, and technology sectors, as well as Wall Street’s cautious stance and bond market adjustments ahead of the U.S. presidential election. Let’s explore these topics in detail.

U.S. October Non-Farm Payrolls Show Mixed Signals

The October Non-Farm Payrolls report showed a modest addition of 12,000 jobs, well below the forecasted 113,000. Contributing factors included hurricanes affecting the southern U.S. coast and significant strikes in industries like Boeing. Despite the limited job growth, average hourly earnings rose 0.4%, translating to a 4% year-over-year increase, while the unemployment rate held steady at 4.1%. This weaker-than-expected report has spurred speculation of a 25 basis point rate cut by the Federal Reserve, as it considers the broader economic context.

Investment Insight: Slowing job growth may support a near-term rate cut, which could impact rate-sensitive assets. Investors should monitor upcoming Fed decisions, as these could influence market conditions broadly.

Volkswagen CEO Emphasizes Cost-Cutting Amid Structural Challenges

Volkswagen CEO Oliver Blume has outlined a significant cost-cutting plan to tackle long-standing structural inefficiencies. Blume cited “decades of structural problems” as key drivers behind the decision to pursue €4 billion in savings. The strategy may involve workforce reductions and potential plant closures as VW navigates high production demands and rising restructuring costs. This move aims to position VW more competitively, particularly in its transition to electric vehicles and compliance with regulatory requirements.

Investment Insight: VW’s restructuring plan may lead to near-term volatility, but its focus on cost savings could enhance long-term financial stability. Investors should watch for developments that could strengthen VW’s competitiveness.

Market Price: Volkswagen AG (VOW.DE): €91.20

Nvidia Requests Early Delivery of Next-Gen HBM4 Chips

Nvidia CEO Jensen Huang has asked SK Hynix to expedite the supply of its next-generation HBM4 memory chips by six months, reflecting the high demand for AI-compatible hardware. Originally set for release in the second half of 2025, the accelerated timeline supports Nvidia’s dominant position in the AI chip market, where it holds over 80% market share. Following the announcement, SK Hynix shares rose by 5.1%, underscoring strong investor interest in high-bandwidth memory for AI applications and the competitive race among chip suppliers.

Investment Insight: Nvidia’s chip demand signals growth opportunities in AI and semiconductor sectors. Investors may look to companies focused on high-performance computing for exposure to this trend.

Market Price: Nvidia (NVDA): $139.34

Buffett Reduces Apple Stake Amid Market Adjustments

Berkshire Hathaway continued trimming its Apple holdings in Q3, reducing its stake by 25%, following a nearly 50% cut in Q2. Despite this, Apple remains Berkshire’s largest holding, suggesting Buffett’s adjustment may be tied to portfolio rebalancing or tax strategies. Berkshire’s cash reserves now stand at a record $325.2 billion, with $34.6 billion in equities sold this quarter, indicating a shift toward liquidity and cautious positioning.

Investment Insight: Berkshire’s stake reduction in Apple could reflect a broader cautious approach. Investors should keep an eye on Berkshire’s moves, as they may indicate broader market sentiment shifts.

Market Price: Apple (AAPL): $222.91

Wall Street Eyes Election, Avoids Big Bets Amid Volatility

With the U.S. presidential election approaching, Wall Street is adopting a cautious stance, refraining from bold moves due to anticipated volatility. The Cboe Volatility Index has climbed as investors hedge against potential post-election market swings. Sectors such as financials, renewable energy, and crypto are seeing defensive options trades, while currency markets brace for fluctuations in the yuan, peso, and euro, anticipating potential shifts in trade policies post-election.

Investment Insight: Rising volatility and caution on Wall Street reflect the uncertain pre-election environment. Investors might consider defensive strategies or hedging options as the election nears.

Bond Traders Pare Back Ahead of Pivotal Week

Bond traders are reducing positions in anticipation of the U.S. election and a likely Federal Reserve rate cut. Treasury yields have been volatile, with traders avoiding significant positions due to the election’s potential impact on fiscal policy. A Republican sweep could push yields higher, while a Democratic win or divided government might bring relief to bondholders. Current volatility in the bond market is the highest seen this year, signaling a cautious outlook.

Investment Insight: Bond market adjustments highlight uncertainty over fiscal policies. Investors should remain attuned to bond market movements as the election outcome becomes clearer.

Asian Markets Rise as China Begins Economic Meeting

Asian shares rose as China began a key economic meeting, sparking optimism for potential fiscal stimulus. Markets in Hong Kong and Shanghai gained on expectations of supportive measures, while South Korea’s Kospi and Australia’s ASX 200 also saw gains. In the U.S., stock futures edged higher following a Friday rally, driven by strong earnings from Amazon and Intel. Meanwhile, oil prices rose over 1% after OPEC+ extended production cuts, with U.S. crude at $70.68 per barrel and Brent at $74.25.

Investment Insight: China’s potential stimulus plans could positively affect global markets, particularly in Asia. However, investors should remain cautious, given the election’s potential impact on international markets.

Market Price:

Brent Crude: $74.25 per barrel

U.S. crude: $70.55 per barrel

Hang Seng Index: HKD 20,561.78

Conclusion

These developments across sectors illustrate the potential for significant shifts based on upcoming events, particularly the U.S. election. Staying informed will be essential for navigating these uncertainties.

Upcoming Dates to Watch

- November 7, 2024: U.S. Federal Reserve interest rate decision.

- November 14, 2024: Eurozone Q3 GDP report release.

- November 13, 2024: U.S. Consumer Price Index (CPI) data release.

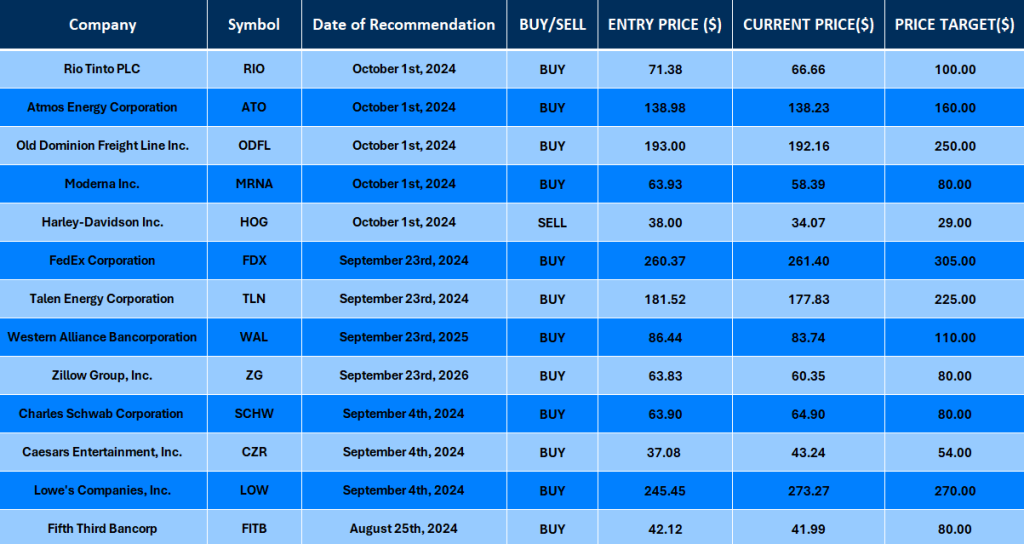

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.