Date Issued – 9th December 2024

Preview

Asian markets slid on Monday as South Korea’s Kospi dropped 2.3% amid political strife, and Chinese shares fell ahead of key economic meetings. Tokyo’s Nikkei edged higher on expectations of a Bank of Japan rate hike, while U.S. equities hit record highs last week, buoyed by strong jobs data that raised hopes for a Fed rate cut. Oil prices rose slightly amid Middle East concerns, though weak Chinese demand and oversupply weigh on the outlook. Meanwhile, China’s inflation slowed to 0.2% in November, reflecting ongoing economic fragility as Beijing prepares for pivotal policy announcements. In Japan, Kioxia’s $5.2 billion IPO underscores growing interest in tech, driven by AI demand, despite NAND pricing pressures. In the U.S., November saw 227,000 new jobs, beating expectations, with wage growth solid at 4% year-over-year. While labor market resilience supports consumer spending, all eyes remain on the Fed’s Dec. 18 rate decision. Investors are urged to track geopolitical risks, stimulus measures, and central bank policies for emerging opportunities.

Asian Markets Slide Amid Political and Economic Uncertainty

Asian shares dropped on Monday, with South Korea’s Kospi tumbling 2.3% amid ongoing domestic political turmoil and global market uncertainty. Chinese shares also fell ahead of a key economic planning meeting, while Tokyo’s Nikkei rose slightly on expectations of a potential Bank of Japan rate hike. Meanwhile, U.S. equities ended last week at record highs, buoyed by robust jobs data that bolstered hopes for a Federal Reserve rate cut. Oil prices saw mixed movements, and Bitcoin hovered near $99,600 after a record-breaking surge.

Investment Insight: Asian market volatility underscores the importance of monitoring geopolitical risks and central bank policy shifts. U.S. markets, buoyed by strong jobs data, remain a beacon of stability, but caution is warranted as the Federal Reserve navigates rate adjustments.

China’s Inflation Slows Ahead of Pivotal Economic Meetings

China’s consumer inflation eased to 0.2% in November, its lowest since June, while factory deflation moderated, marking 26 consecutive months of decline. The mixed data reflects the limited impact of recent stimulus measures as Beijing prepares for key economic policy meetings this week. Analysts anticipate stronger fiscal and monetary stimulus, including potential rate cuts and expanded subsidies, to counter external pressures like U.S. tariffs and to boost domestic consumption. Stock market reaction was subdued, with the CSI 300 and Hang Seng China Enterprises Index both declining.

Investment Insight: China’s weak inflation signals ongoing economic fragility. Investors should watch for potential policy announcements this week, as greater stimulus and rate cuts could present opportunities in domestic consumption and infrastructure-linked sectors.

Oil Prices Rise Amid Syrian Upheaval and Middle East Uncertainty

Oil prices edged higher on Monday, with Brent nearing $72 a barrel, as markets assessed the implications of the Syrian government’s collapse. The power vacuum in Syria has heightened concerns of regional instability, though analysts believe the risk of widespread oil supply disruptions remains low. Despite geopolitical tensions in the Middle East and Ukraine, crude prices have remained range-bound due to weak Chinese demand and an expected supply glut in 2024. Adding to the bearish outlook, Saudi Aramco cut oil prices for Asia and Europe for January deliveries.

Investment Insight: Geopolitical risks may provide short-term volatility in oil markets, but abundant supply and weak demand are likely to cap upside potential. Investors should focus on regions or sectors less sensitive to oil price fluctuations.

Kioxia Prices $5.2 Billion IPO Amid Surge in Japanese Listings

Bain Capital-backed Kioxia Holdings has priced its IPO at ¥1,455 per share, valuing the memory chipmaker at $5.2 billion. The listing, set for Dec. 18, marks a significant step for the Tokyo-based firm after shelving its 2020 IPO plans due to a prolonged slump in NAND prices. Analysts see potential growth for Kioxia, driven by rising demand from AI-server customers and its advanced NAND and SSD technologies. The IPO comes amid a wave of large Japanese listings, including MBK-backed Kuroda Group’s upcoming debut.

Investment Insight: Kioxia’s IPO highlights rising interest in Japan’s tech sector. Investors should watch for AI-driven demand in memory chips, but note the capital-intensive nature of the industry and ongoing pricing pressures in NAND markets.

US Job Market Rebounds, Adding 227,000 Jobs in November

The US economy added 227,000 jobs in November, surpassing expectations of 220,000, while the unemployment rate rose slightly to 4.2%. The labor market showed resilience after October’s disruptions from hurricanes and labor strikes, with revisions adding 56,000 more jobs to prior months. Wage growth climbed 0.4% month-over-month and 4% year-over-year, outpacing forecasts. Despite a slight dip in labor force participation to 62.5%, the report signals a stable labor market, aligning with Federal Reserve expectations for a soft landing. Markets widely anticipate a Fed rate cut at its Dec. 18 meeting.

Investment Insight: Steady job growth and rising wages support consumer spending but reinforce cautious optimism about a soft landing. Investors should monitor Fed policy shifts, as easing rates could bolster equities but signal caution in fixed-income markets.

Conclusion

Global markets remain at a crossroads as geopolitical tensions, central bank policies, and economic uncertainties drive investor sentiment. Asia faces volatility, with China’s weak inflation and South Korea’s political turmoil weighing on sentiment, while Japan’s IPO boom highlights tech sector opportunities. In the U.S., robust job growth underpins optimism, but caution surrounds the Federal Reserve’s next move. Oil prices reflect a tug-of-war between geopolitical risks and oversupply concerns. As key policy meetings and rate decisions loom, investors should stay vigilant, focusing on sectors poised to benefit from stimulus measures, resilient labor markets, and evolving global demand trends.

Upcoming Dates to Watch

- December 11, 2024: US CPI

- December 12, 2024: US PPI

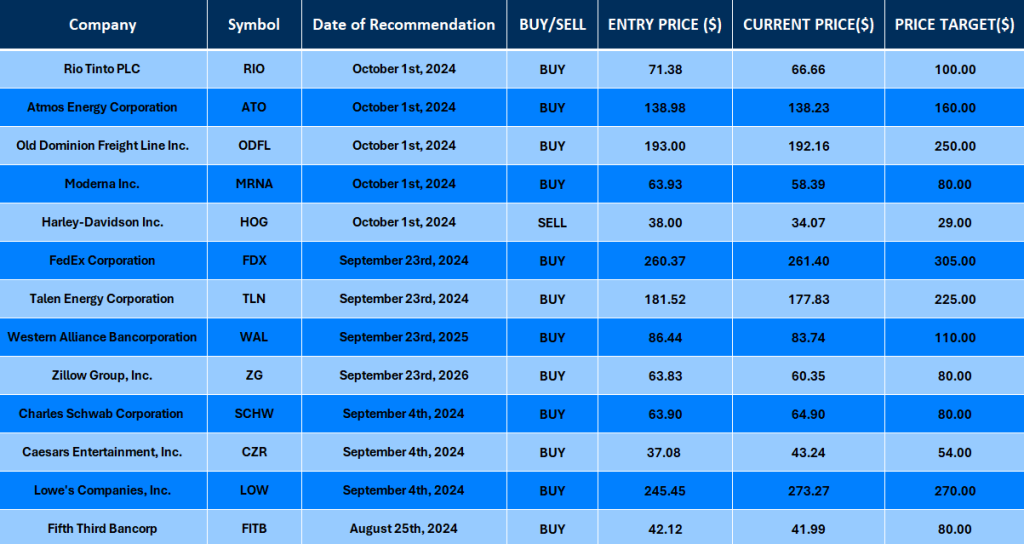

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.