Daily Synopsis of the New York market close

Date Issued – 11th December 2024

Preview

Asian stocks dipped as markets awaited US inflation data, which could shape the Federal Reserve’s rate decision. While South Korean stocks gained, Chinese equities fluctuated amid expectations of fiscal stimulus in 2025. The US dollar steadied, Treasury yields rose, and Japan’s yen strengthened slightly. Separately, SpaceX’s valuation surged to $350 billion after a $1.25 billion insider share sale, solidifying its dominance in space tech. Intel’s credit rating was downgraded by S&P due to sluggish recovery and leadership uncertainty, raising concerns about its turnaround strategy. Meanwhile, US Steel shares plunged 9.7% as President Biden moved to block a $14.1 billion sale to Japan’s Nippon Steel over national security concerns. Lastly, Broadcom’s AI-driven growth lifted its stock price targets ahead of earnings, though order slowdowns may temper near-term momentum. Investors are urged to monitor US CPI data, geopolitical tensions, and sector-specific risks as markets navigate opportunities in semiconductors, space tech, and critical industries.

Asian Stocks Slip as Dollar Holds Steady Ahead of US CPI Data

Asian markets retreated as investors anticipate the release of US inflation data, which could influence the Federal Reserve’s interest rate decision next week. Hong Kong and mainland Chinese stocks fluctuated, while South Korea extended gains following recent political turbulence. Meanwhile, the US dollar steadied after a three-day rally, and US Treasury yields inched higher. China’s Central Economic Work Conference raised expectations of fiscal stimulus for 2025, with economists forecasting the largest budget deficit in decades. In Japan, the yen strengthened slightly as producer price inflation accelerated, but remained subdued ahead of US CPI data.

Investment Insight

Investors should watch US CPI data closely, as it could solidify expectations for upcoming Fed rate cuts. Meanwhile, China’s potential fiscal expansion and Japan’s inflation trends suggest evolving opportunities in Asian markets—but also heightened risks. Diversification remains key.

SpaceX Valuation Soars to $350 Billion in Insider Share Sale

SpaceX has agreed to a $1.25 billion insider share purchase, valuing the company at a staggering $350 billion, according to an internal memo. The per-share price of $185 marks a sharp increase from $112 just three months ago. SpaceX itself will reportedly buy up to $500 million in common stock as part of this transaction, solidifying its position as the world’s most valuable private startup. The valuation underscores SpaceX’s dominance in rocket launches and its growing Starlink internet network, while Elon Musk’s businesses continue to gain momentum post-election, with his personal wealth climbing to $384 billion.

Investment Insight

SpaceX’s valuation jump highlights investor confidence in space technology and satellite communications as high-growth sectors. However, private market dynamics and geopolitical considerations remain key risks for long-term gains in the space industry.

Intel’s Credit Rating Downgraded by S&P on Slow Recovery, Leadership Uncertainty

S&P Global Ratings has downgraded Intel’s credit rating to ‘BBB’ from ‘BBB+’ due to a sluggish recovery and uncertainty following CEO Pat Gelsinger’s unexpected departure. Intel’s revenue of $38.84 billion for the first nine months of 2024 fell short of expectations, raising concerns about the company’s turnaround plan. Gelsinger’s exit before completing his four-year roadmap to reclaim chip leadership from Taiwan Semiconductor Manufacturing Co. adds further uncertainty. Despite the downgrade, S&P maintained a “stable” outlook, citing modest growth prospects in 2025.

Investment Insight

Intel’s credit downgrade highlights risks tied to leadership changes and execution challenges. Investors should assess the company’s ability to stabilize and innovate amid rising competition in the semiconductor space.

Market price: Intel Corp (INTC): USD 20.16

US Steel Shares Plunge as Biden Set to Block Nippon Steel Deal

President Joe Biden is expected to block the $14.1 billion sale of US Steel to Japan’s Nippon Steel on national security grounds, following a recommendation from the Committee on Foreign Investment in the United States (CFIUS). The deal has faced political opposition, with Biden emphasizing the need for US Steel to remain domestically owned. US Steel warned of potential headquarters relocation and operational closures if the merger fails, while Nippon Steel criticized the politicization of the process. Shares of US Steel dropped 9.7% on the news, while Nippon Steel shares remained steady.

Investment Insight

The blocked merger underlines the growing scrutiny of cross-border deals in critical industries. Investors should monitor geopolitical tensions and protectionist policies, which could weigh on M&A activity and valuations in sectors tied to national security.

Broadcom Targets AI Growth as Analysts Raise Price Expectations Pre-Earnings

Broadcom’s stock price target has been raised by Citi to $205 ahead of its fiscal Q4 earnings, driven by strong AI semiconductor growth and VMware’s integration. Analysts expect Q4 revenue to hit $14.06 billion, a 51% year-over-year increase. Broadcom’s AI chip sales are forecasted to reach $12 billion in 2024, with partnerships like Apple and Google supporting growth. However, a slowdown in Google orders could temper Q1 guidance, offset by expected business from Meta in 2025. Broadcom shares are up 54% year-to-date, reflecting bullish market sentiment.

Investment Insight

Broadcom’s AI-driven growth positions it as a long-term tech leader, but near-term headwinds like order slowdowns warrant caution. Investors should focus on its ability to sustain momentum in the competitive AI infrastructure market.

Market Price: Broadcom Inc (AVGO): USD 171.81

Conclusion

In a week dominated by anticipation of US inflation data, markets are grappling with shifting dynamics across sectors. Asian stocks wavered as fiscal stimulus in China and Japan’s inflation trends hint at evolving opportunities. SpaceX’s soaring valuation underscores investor confidence in space tech, while Intel’s downgrade highlights challenges in leadership and execution. The blocked US Steel deal reflects growing geopolitical tensions, adding uncertainty to cross-border M&A. Meanwhile, Broadcom’s AI momentum signals long-term promise despite near-term risks. As markets await clarity from the Fed, diversification and vigilance remain essential in navigating economic shifts and sector-specific opportunities.

Upcoming Dates to Watch

- December 11, 2024: US CPI

- December 12, 2024: US PPI

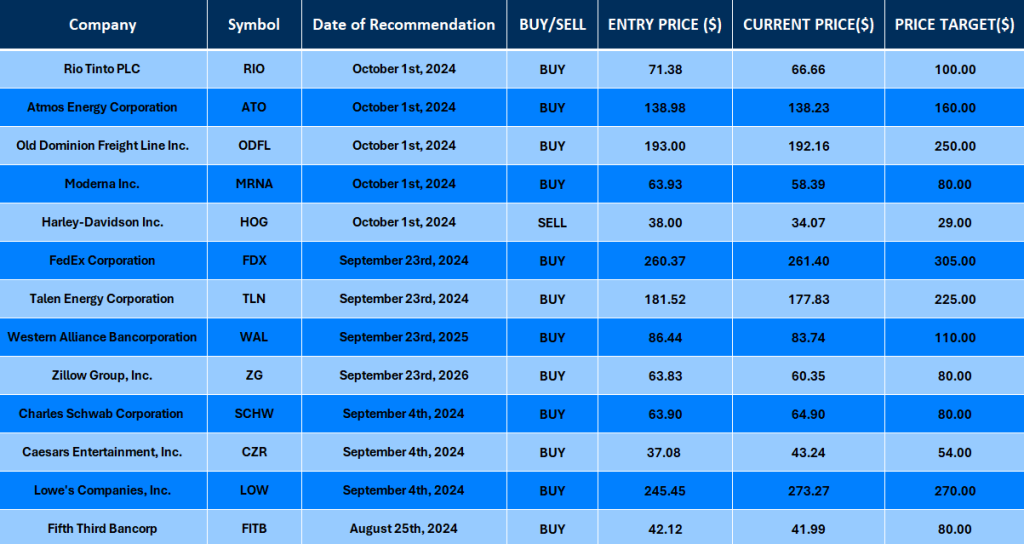

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.

Daily Synopsis of the New York market close

Date Issued – 9th December 2024

Preview

Asian markets slid on Monday as South Korea’s Kospi dropped 2.3% amid political strife, and Chinese shares fell ahead of key economic meetings. Tokyo’s Nikkei edged higher on expectations of a Bank of Japan rate hike, while U.S. equities hit record highs last week, buoyed by strong jobs data that raised hopes for a Fed rate cut. Oil prices rose slightly amid Middle East concerns, though weak Chinese demand and oversupply weigh on the outlook. Meanwhile, China’s inflation slowed to 0.2% in November, reflecting ongoing economic fragility as Beijing prepares for pivotal policy announcements. In Japan, Kioxia’s $5.2 billion IPO underscores growing interest in tech, driven by AI demand, despite NAND pricing pressures. In the U.S., November saw 227,000 new jobs, beating expectations, with wage growth solid at 4% year-over-year. While labor market resilience supports consumer spending, all eyes remain on the Fed’s Dec. 18 rate decision. Investors are urged to track geopolitical risks, stimulus measures, and central bank policies for emerging opportunities.

Asian Markets Slide Amid Political and Economic Uncertainty

Asian shares dropped on Monday, with South Korea’s Kospi tumbling 2.3% amid ongoing domestic political turmoil and global market uncertainty. Chinese shares also fell ahead of a key economic planning meeting, while Tokyo’s Nikkei rose slightly on expectations of a potential Bank of Japan rate hike. Meanwhile, U.S. equities ended last week at record highs, buoyed by robust jobs data that bolstered hopes for a Federal Reserve rate cut. Oil prices saw mixed movements, and Bitcoin hovered near $99,600 after a record-breaking surge.

Investment Insight: Asian market volatility underscores the importance of monitoring geopolitical risks and central bank policy shifts. U.S. markets, buoyed by strong jobs data, remain a beacon of stability, but caution is warranted as the Federal Reserve navigates rate adjustments.

China’s Inflation Slows Ahead of Pivotal Economic Meetings

China’s consumer inflation eased to 0.2% in November, its lowest since June, while factory deflation moderated, marking 26 consecutive months of decline. The mixed data reflects the limited impact of recent stimulus measures as Beijing prepares for key economic policy meetings this week. Analysts anticipate stronger fiscal and monetary stimulus, including potential rate cuts and expanded subsidies, to counter external pressures like U.S. tariffs and to boost domestic consumption. Stock market reaction was subdued, with the CSI 300 and Hang Seng China Enterprises Index both declining.

Investment Insight: China’s weak inflation signals ongoing economic fragility. Investors should watch for potential policy announcements this week, as greater stimulus and rate cuts could present opportunities in domestic consumption and infrastructure-linked sectors.

Oil Prices Rise Amid Syrian Upheaval and Middle East Uncertainty

Oil prices edged higher on Monday, with Brent nearing $72 a barrel, as markets assessed the implications of the Syrian government’s collapse. The power vacuum in Syria has heightened concerns of regional instability, though analysts believe the risk of widespread oil supply disruptions remains low. Despite geopolitical tensions in the Middle East and Ukraine, crude prices have remained range-bound due to weak Chinese demand and an expected supply glut in 2024. Adding to the bearish outlook, Saudi Aramco cut oil prices for Asia and Europe for January deliveries.

Investment Insight: Geopolitical risks may provide short-term volatility in oil markets, but abundant supply and weak demand are likely to cap upside potential. Investors should focus on regions or sectors less sensitive to oil price fluctuations.

Kioxia Prices $5.2 Billion IPO Amid Surge in Japanese Listings

Bain Capital-backed Kioxia Holdings has priced its IPO at ¥1,455 per share, valuing the memory chipmaker at $5.2 billion. The listing, set for Dec. 18, marks a significant step for the Tokyo-based firm after shelving its 2020 IPO plans due to a prolonged slump in NAND prices. Analysts see potential growth for Kioxia, driven by rising demand from AI-server customers and its advanced NAND and SSD technologies. The IPO comes amid a wave of large Japanese listings, including MBK-backed Kuroda Group’s upcoming debut.

Investment Insight: Kioxia’s IPO highlights rising interest in Japan’s tech sector. Investors should watch for AI-driven demand in memory chips, but note the capital-intensive nature of the industry and ongoing pricing pressures in NAND markets.

US Job Market Rebounds, Adding 227,000 Jobs in November

The US economy added 227,000 jobs in November, surpassing expectations of 220,000, while the unemployment rate rose slightly to 4.2%. The labor market showed resilience after October’s disruptions from hurricanes and labor strikes, with revisions adding 56,000 more jobs to prior months. Wage growth climbed 0.4% month-over-month and 4% year-over-year, outpacing forecasts. Despite a slight dip in labor force participation to 62.5%, the report signals a stable labor market, aligning with Federal Reserve expectations for a soft landing. Markets widely anticipate a Fed rate cut at its Dec. 18 meeting.

Investment Insight: Steady job growth and rising wages support consumer spending but reinforce cautious optimism about a soft landing. Investors should monitor Fed policy shifts, as easing rates could bolster equities but signal caution in fixed-income markets.

Conclusion

Global markets remain at a crossroads as geopolitical tensions, central bank policies, and economic uncertainties drive investor sentiment. Asia faces volatility, with China’s weak inflation and South Korea’s political turmoil weighing on sentiment, while Japan’s IPO boom highlights tech sector opportunities. In the U.S., robust job growth underpins optimism, but caution surrounds the Federal Reserve’s next move. Oil prices reflect a tug-of-war between geopolitical risks and oversupply concerns. As key policy meetings and rate decisions loom, investors should stay vigilant, focusing on sectors poised to benefit from stimulus measures, resilient labor markets, and evolving global demand trends.

Upcoming Dates to Watch

- December 11, 2024: US CPI

- December 12, 2024: US PPI

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.

Daily Synopsis of the New York market close

Date Issued – 6th December 2024

Preview

The November jobs report is expected to show a rebound in hiring, with payrolls forecasted to rise by 215,000 after October’s hurricane- and strike-affected 12,000. Unemployment is projected to hold at 4.1%, while wage growth may hit 3.9% year-over-year. Post-hurricane recovery and strike resolutions, including at Boeing, are driving the rebound, with job openings at 7.74 million reflecting a tight labor market. Meanwhile, Chinese stocks rallied on stimulus hopes ahead of a key policy meeting, while the Reserve Bank of India held rates steady but cut the cash reserve ratio to ease liquidity pressures amid rising inflation. Bitcoin faced volatility, dropping 7% after its surge past $100,000, as traders took profits. In corporate news, Hewlett Packard Enterprise beat expectations with robust AI server demand driving a 32% sales increase, though its networking segment declined. These developments underscore resilient labor markets, cautious central bank policies, crypto volatility, and rising demand for AI infrastructure, with implications for inflation, Fed policy, and global investment strategies.

November Jobs Report Expected to Reflect Rebound Amid Post-Hurricane Recovery

The November jobs report is forecasted to show a significant hiring rebound, with nonfarm payrolls expected to rise by 215,000 following October’s hurricane- and strike-impacted figure of just 12,000. The unemployment rate is projected to hold steady at 4.1%. Goldman Sachs economists attribute the anticipated rebound to post-hurricane recovery and the resolution of worker strikes, including at Boeing. Key metrics to watch include wage growth, expected to rise 3.9% year-over-year, and average weekly hours worked, which are predicted to remain flat at 34.3. Meanwhile, labor market data shows job openings climbed to 7.74 million in October, reflecting a modestly tight labor market.

Investment Insight

The November jobs report will likely reinforce expectations of a resilient labor market, easing recession fears and supporting the Federal Reserve’s measured approach to rate cuts. Investors should monitor wage growth trends, as they could signal future inflationary pressures impacting Fed policy.

Gold Bulls Gain Momentum as Macquarie Raises 2025 Forecasts

Macquarie Group has raised its gold price forecasts for 2025, predicting the metal could hit record highs as the Federal Reserve cuts rates and central banks continue stockpiling bullion. Analysts see potential for gold to “quickly challenge” $3,000 an ounce, especially if Chinese demand rises or if President-elect Donald Trump’s fiscal policies weaken the US outlook.

While gold may face headwinds from a stronger dollar in early 2025, it’s expected to average $2,800 an ounce in the second quarter, up 12% from prior estimates. This year, gold has surged 28%, driven by central bank buying, a Fed pivot to rate cuts, and a rebound in ETF demand. Macquarie notes ETF holdings remain 25% below 2020 highs, leaving room for further accumulation if conditions favor gold.

Investment Insight

Gold remains a compelling hedge against economic uncertainty and lower interest rates. However, investors should monitor dollar strength and shifting central bank policies, as these could temper the metal’s rally in the long term.

South Korea’s Ruling Party Moves to Block Presidential Impeachment

South Korea’s People Power Party (PPP) is rallying to block an impeachment motion against President Yoon Suk Yeol, which could be voted on as early as Saturday. PPP leader Han Dong-hoon urged party members to reject the motion, signaling efforts to distance the party from Yoon while maintaining conservative unity.

This comes after Yoon faced backlash for a short-lived martial law declaration on Tuesday, which was swiftly overturned by parliament. The opposition, accusing Yoon and his former defense chief Kim Yong-hyun of treason, needs a two-thirds majority (200 votes) to pass the motion—requiring support from some ruling party lawmakers. Yoon has remained silent as the political crisis unfolds.

Investment Insight

Political instability in South Korea could weigh on investor confidence, particularly in domestic equities and the won. However, markets may stabilize if the ruling party successfully blocks impeachment and restores political cohesion.

Salesforce Analysts Boost Price Targets After AI-Driven Results

Salesforce shares rallied as analysts raised their price targets following its fiscal Q3 report. The company posted $9.44 billion in revenue, beating estimates, but fell short on earnings per share ($2.41 vs. $2.44 expected). CEO Marc Benioff highlighted Salesforce’s AI platform, Agentforce, as a transformative tool for automating business processes, calling it the start of a “digital labor revolution.”

Despite strong early demand for Agentforce, Salesforce’s Q4 guidance ($9.9–$10.1 billion) fell slightly below Wall Street expectations. Wedbush raised its target to $425, citing AI growth potential, while other analysts noted steady—though unspectacular—revenue growth. Shares are up 37% YTD, with investors betting on Agentforce’s long-term impact despite near-term skepticism.

Investment Insight

Salesforce’s AI narrative is compelling, but current growth remains modest. Investors should weigh long-term AI-driven potential against near-term execution risks, particularly given conservative guidance. Avoid chasing the rally without clarity on sustained growth metrics.

Market price: Salesforce (CRM): USD 367.87

Korea Zinc Surges 270% Amid Proxy Battle, Analysts See Risks Ahead

Korea Zinc shares have soared nearly 270% year-to-date, making it the top performer on MSCI’s global equity index. The stock surged 12% on Thursday, driven by investor speculation ahead of a heated proxy battle between its largest shareholder, Young Poong Corp., and Chairman Yun B. Choi. The January 23 vote could determine control of the board, with each share potentially influencing the outcome.

Despite the rally, analysts warn the valuation is unsustainable, trading at nearly double the median among global peers. Bloomberg data predicts a potential 66% drop in the stock’s price within 12 months, though it still holds 14 buy ratings.

Investment Insight

Korea Zinc’s meteoric rise reflects speculative fervor tied to the proxy battle, not fundamentals. Investors should tread cautiously, as valuations suggest a high risk of sharp correction once the management dispute concludes.

Market price: Korea Zinc Inc (KRZ 010130): KRW 1,954,000.00

Conclusion

The week’s developments highlight the volatile mix of opportunity and risk across global markets. Bitcoin’s surge past $100,000 reflects growing optimism toward crypto-friendly policies, while gold’s upward trajectory underscores its role as a hedge against economic uncertainty.

In South Korea, political instability adds caution to investor sentiment, as Salesforce’s AI-driven ambitions spark debate over near-term execution versus long-term potential. Korea Zinc’s meteoric rise serves as a stark reminder of speculative risks in overheated markets. As regulatory shifts, political turbulence, and technological innovation shape the landscape, investors must stay vigilant, balancing momentum-driven rallies with the potential for sharp corrections.

Upcoming Dates to Watch

- December 6, 2024: US Consumer Sentiment

- December 11, 2024: US CPI

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.

Daily Synopsis of the New York market close

Date Issued – 5th December 2024

Preview

Bitcoin has surpassed $100,000 for the first time after President-elect Donald Trump nominated crypto-friendly Paul Atkins as SEC chair. This fueled a $1.3 trillion crypto market rally. Bitcoin ETFs have drawn $8 billion in inflows, despite Mt. Gox moving $2.4 billion in Bitcoin.

Meanwhile, gold forecasts rose sharply, with Macquarie predicting record highs of $3,000 an ounce by 2025 amid central bank buying and Federal Reserve rate cuts. In South Korea, political tensions escalate as the ruling party seeks to block President Yoon Suk Yeol’s impeachment, raising investor concerns.

Salesforce shares climbed after AI-driven results, though conservative Q4 guidance tempered optimism. Korea Zinc’s 270% year-to-date surge, driven by a looming proxy battle, has analysts warning of a sharp correction due to unsustainable valuations. Investors across markets are weighing opportunities against risks as volatility remains a key theme.

Bitcoin Tops $100,000 After Trump’s Pro-Crypto SEC Pick

President-elect Donald Trump’s nomination of Paul Atkins, a crypto-friendly regulator, as the next SEC chair has propelled Bitcoin past the $100,000 mark for the first time. Bitcoin surged 6.1% to $103,801 on Thursday before stabilizing at $103,420 in Singapore. The broader crypto market has gained $1.3 trillion since Trump’s election, fueled by hopes for regulatory leniency and a national embrace of digital assets.

Analysts see this as a “momentum rally,” with Bitcoin ETFs attracting over $8 billion in inflows since the election. Meanwhile, the bankrupt Mt. Gox exchange moved $2.4 billion in Bitcoin, but traders shrugged off potential concerns about a supply overhang. Other digital assets showed mixed performance, with Dogecoin rising and Ether steady.

Investment Insight

Bitcoin’s six-figure milestone signals growing institutional interest, but its speculative nature remains a risk. While regulatory tailwinds could drive further gains, investors should brace for volatility and avoid chasing the rally blindly.

Gold Bulls Gain Momentum as Macquarie Raises 2025 Forecasts

Macquarie Group has raised its gold price forecasts for 2025, predicting the metal could hit record highs as the Federal Reserve cuts rates and central banks continue stockpiling bullion. Analysts see potential for gold to “quickly challenge” $3,000 an ounce, especially if Chinese demand rises or if President-elect Donald Trump’s fiscal policies weaken the US outlook.

While gold may face headwinds from a stronger dollar in early 2025, it’s expected to average $2,800 an ounce in the second quarter, up 12% from prior estimates. This year, gold has surged 28%, driven by central bank buying, a Fed pivot to rate cuts, and a rebound in ETF demand. Macquarie notes ETF holdings remain 25% below 2020 highs, leaving room for further accumulation if conditions favor gold.

Investment Insight

Gold remains a compelling hedge against economic uncertainty and lower interest rates. However, investors should monitor dollar strength and shifting central bank policies, as these could temper the metal’s rally in the long term.

South Korea’s Ruling Party Moves to Block Presidential Impeachment

South Korea’s People Power Party (PPP) is rallying to block an impeachment motion against President Yoon Suk Yeol, which could be voted on as early as Saturday. PPP leader Han Dong-hoon urged party members to reject the motion, signaling efforts to distance the party from Yoon while maintaining conservative unity.

This comes after Yoon faced backlash for a short-lived martial law declaration on Tuesday, which was swiftly overturned by parliament. The opposition, accusing Yoon and his former defense chief Kim Yong-hyun of treason, needs a two-thirds majority (200 votes) to pass the motion—requiring support from some ruling party lawmakers. Yoon has remained silent as the political crisis unfolds.

Investment Insight

Political instability in South Korea could weigh on investor confidence, particularly in domestic equities and the won. However, markets may stabilize if the ruling party successfully blocks impeachment and restores political cohesion.

Salesforce Analysts Boost Price Targets After AI-Driven Results

Salesforce shares rallied as analysts raised their price targets following its fiscal Q3 report. The company posted $9.44 billion in revenue, beating estimates, but fell short on earnings per share ($2.41 vs. $2.44 expected). CEO Marc Benioff highlighted Salesforce’s AI platform, Agentforce, as a transformative tool for automating business processes, calling it the start of a “digital labor revolution.”

Despite strong early demand for Agentforce, Salesforce’s Q4 guidance ($9.9–$10.1 billion) fell slightly below Wall Street expectations. Wedbush raised its target to $425, citing AI growth potential, while other analysts noted steady—though unspectacular—revenue growth. Shares are up 37% YTD, with investors betting on Agentforce’s long-term impact despite near-term skepticism.

Investment Insight

Salesforce’s AI narrative is compelling, but current growth remains modest. Investors should weigh long-term AI-driven potential against near-term execution risks, particularly given conservative guidance. Avoid chasing the rally without clarity on sustained growth metrics.

Market price: Salesforce (CRM): USD 367.87

Korea Zinc Surges 270% Amid Proxy Battle, Analysts See Risks Ahead

Korea Zinc shares have soared nearly 270% year-to-date, making it the top performer on MSCI’s global equity index. The stock surged 12% on Thursday, driven by investor speculation ahead of a heated proxy battle between its largest shareholder, Young Poong Corp., and Chairman Yun B. Choi. The January 23 vote could determine control of the board, with each share potentially influencing the outcome.

Despite the rally, analysts warn the valuation is unsustainable, trading at nearly double the median among global peers. Bloomberg data predicts a potential 66% drop in the stock’s price within 12 months, though it still holds 14 buy ratings.

Investment Insight

Korea Zinc’s meteoric rise reflects speculative fervor tied to the proxy battle, not fundamentals. Investors should tread cautiously, as valuations suggest a high risk of sharp correction once the management dispute concludes.

Market price: Korea Zinc Inc (KRZ 010130): KRW 1,954,000.00

Conclusion

The week’s developments highlight the volatile mix of opportunity and risk across global markets. Bitcoin’s surge past $100,000 reflects growing optimism toward crypto-friendly policies, while gold’s upward trajectory underscores its role as a hedge against economic uncertainty.

In South Korea, political instability adds caution to investor sentiment, as Salesforce’s AI-driven ambitions spark debate over near-term execution versus long-term potential. Korea Zinc’s meteoric rise serves as a stark reminder of speculative risks in overheated markets. As regulatory shifts, political turbulence, and technological innovation shape the landscape, investors must stay vigilant, balancing momentum-driven rallies with the potential for sharp corrections.

Upcoming Dates to Watch

- December 6, 2024: US Consumer Sentiment

- December 11, 2024: US CPI

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.

Daily Synopsis of the New York market close

Date Issued – 4th December 2024

Preview

France faces deepening political and economic challenges as Prime Minister Michel Barnier’s government nears collapse over austerity disputes, denting business confidence and raising concerns about economic fragility, though fears of a sovereign debt crisis remain muted. In South Korea, markets were rattled by President Yoon Suk Yeol’s brief martial law declaration amid impeachment efforts, with the Kospi down 2.3% and political instability exacerbating the “Korea Discount.” Meanwhile, China plans to quadruple its nuclear capacity by 2035, surpassing global leaders, though safety and regulatory risks could temper growth as private capital reforms take shape. Salesforce shares surged 10% after beating revenue forecasts, driven by AI-driven products that signal future growth despite challenges in acquired units. Lastly, Lynas Rare Earths rallied on China’s mineral export ban, underscoring opportunities for non-Chinese suppliers as geopolitical tensions drive demand for critical minerals.

France’s Political Crisis Rattles Markets, But No Sovereign Debt Meltdown Yet

France faces mounting economic and political challenges as Prime Minister Michel Barnier’s government appears poised to collapse following a dispute over austerity measures. Bond markets, while showing signs of strain, have not reached crisis levels. France’s risk premium recently spiked to its highest since 2012, signaling investor unease, but analysts suggest the situation lacks the ingredients for a full-blown sovereign debt crisis. However, political uncertainty is already weighing on businesses, consumer confidence, and future fiscal policies, amplifying concerns about France’s economic fragility amidst broader European challenges.

Investment Insight: While French bonds remain under pressure, many investors see the turmoil as a slow-burning crisis rather than an immediate collapse. Elevated political risks may widen spreads further, but falling ECB rate expectations could offset near-term borrowing costs, presenting selective opportunities for risk-tolerant investors.

Korean Markets Shaken by Yoon’s Martial Law Decree Amid Political Uncertainty

South Korea’s financial markets faced turbulence after President Yoon Suk Yeol briefly declared martial law, sparking political chaos. The won recovered 1.6% after overnight losses, but the Kospi fell by 2.3%, with volatility hitting a three-month high. Credit default swaps widened, signaling increased risk perception. The political turmoil, driven by opposition efforts to impeach Yoon, undermines South Korea’s drive for developed market status and erodes investor confidence in the government’s economic reforms. Banks and Yoon-linked stocks saw sharp declines, while retail investors shifted toward opposition-related meme stocks.

Investment Insight: Political instability adds to South Korea’s “Korea Discount,” keeping valuations low despite global ambitions. While short-term rebounds may emerge with swift resolution, long-term structural and governance concerns will likely persist, limiting upside potential for investors.

Market price: KOSPI: KRW 2464.00

China Accelerates Nuclear Expansion, Eyes Global Leadership

China is set to approve up to 100 new nuclear reactors over the next decade, aiming to quadruple its atomic power capacity to 200 gigawatts by 2035, according to the Chinese Nuclear Society. This rapid growth would make China the world’s largest nuclear power generator by the end of the decade, surpassing the US and France. Despite safety and infrastructure challenges, Beijing’s push aligns with its decarbonization goals and positions it as a major exporter of nuclear technology, particularly the Hualong One reactor. Private capital will likely play a larger role as the capital-intensive sector seeks to maintain momentum.

Investment Insight: China’s nuclear expansion offers opportunities in state-backed firms and emerging private investments. However, safety risks, regulatory hurdles, and inland development challenges may temper long-term growth. Investors should monitor reforms enabling private capital’s larger role in this capital-heavy sector.

Salesforce Surpasses Revenue Estimates, Betting Big on AI

Salesforce posted an 8.3% revenue jump to $9.44 billion in the latest quarter, topping analysts’ expectations and sending shares up 10% in extended trading. The company’s adjusted operating margin hit 33.1%, beating forecasts, as its AI-driven “Agentforce” product begins to reshape its growth narrative. While AI deals are still in early stages, CEO Marc Benioff expressed confidence, announcing plans to hire 1,000 more employees for AI sales. Despite headwinds in acquired units like Slack and Mulesoft, Salesforce maintains strong momentum, projecting revenue of up to $10.1 billion in the current quarter.

Investment Insight: Salesforce’s pivot to AI signals long-term growth potential despite near-term challenges. Strong profitability metrics and optimism around Agentforce could sustain investor interest, though slowing growth in acquired units warrants cautious monitoring.

Lynas Shares Surge as China’s Mineral Export Ban Escalates Trade Tensions

Shares of Lynas Rare Earths jumped 5% to a near three-week high after China banned exports of key minerals—gallium, germanium, and antimony—to the U.S., intensifying trade tensions. The move has sparked fears of broader restrictions on critical minerals like rare earths, nickel, and cobalt. As the largest rare earth producer outside China, Lynas is well-positioned to benefit from growing demand amid geopolitical uncertainty. Analysts suggest Australia could capitalize on its critical mineral exports as global supply chains seek diversification.

Investment Insight: China’s export ban underscores the strategic importance of critical minerals, boosting non-Chinese suppliers like Lynas. Rising trade tensions could drive long-term demand for Australian rare earths, presenting growth opportunities for investors in the sector.

Market price: Lynas Rare Earth Ltd. (LYC.AX): AUD 7.32

Conclusion

France’s political turmoil, South Korea’s instability, and China’s nuclear ambitions highlight the growing interplay between politics and markets, as investors navigate a landscape shaped by uncertainty and opportunity. France’s bond market strains, South Korea’s “Korea Discount,” and China’s push for nuclear dominance all underscore the importance of strategic positioning amid shifting risks. Meanwhile, Salesforce’s AI-driven momentum and Lynas Rare Earths’ gains from escalating trade tensions demonstrate how innovation and geopolitics are reshaping investment narratives. As global markets respond to evolving challenges, selective opportunities emerge for investors willing to balance short-term volatility with long-term growth potential.

Upcoming Dates to Watch

- December 6, 2024: US Consumer Sentiment

- December 11, 2024: US CPI

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.

Daily Synopsis of the New York market close

Date Issued – 4th November 2024

Preview

Today’s newsletter covers impactful developments across labor, automotive, and technology sectors, as well as Wall Street’s cautious stance and bond market adjustments ahead of the U.S. presidential election. Let’s explore these topics in detail.

U.S. October Non-Farm Payrolls Show Mixed Signals

The October Non-Farm Payrolls report showed a modest addition of 12,000 jobs, well below the forecasted 113,000. Contributing factors included hurricanes affecting the southern U.S. coast and significant strikes in industries like Boeing. Despite the limited job growth, average hourly earnings rose 0.4%, translating to a 4% year-over-year increase, while the unemployment rate held steady at 4.1%. This weaker-than-expected report has spurred speculation of a 25 basis point rate cut by the Federal Reserve, as it considers the broader economic context.

Investment Insight: Slowing job growth may support a near-term rate cut, which could impact rate-sensitive assets. Investors should monitor upcoming Fed decisions, as these could influence market conditions broadly.

Volkswagen CEO Emphasizes Cost-Cutting Amid Structural Challenges

Volkswagen CEO Oliver Blume has outlined a significant cost-cutting plan to tackle long-standing structural inefficiencies. Blume cited “decades of structural problems” as key drivers behind the decision to pursue €4 billion in savings. The strategy may involve workforce reductions and potential plant closures as VW navigates high production demands and rising restructuring costs. This move aims to position VW more competitively, particularly in its transition to electric vehicles and compliance with regulatory requirements.

Investment Insight: VW’s restructuring plan may lead to near-term volatility, but its focus on cost savings could enhance long-term financial stability. Investors should watch for developments that could strengthen VW’s competitiveness.

Market Price: Volkswagen AG (VOW.DE): €91.20

Nvidia Requests Early Delivery of Next-Gen HBM4 Chips

Nvidia CEO Jensen Huang has asked SK Hynix to expedite the supply of its next-generation HBM4 memory chips by six months, reflecting the high demand for AI-compatible hardware. Originally set for release in the second half of 2025, the accelerated timeline supports Nvidia’s dominant position in the AI chip market, where it holds over 80% market share. Following the announcement, SK Hynix shares rose by 5.1%, underscoring strong investor interest in high-bandwidth memory for AI applications and the competitive race among chip suppliers.

Investment Insight: Nvidia’s chip demand signals growth opportunities in AI and semiconductor sectors. Investors may look to companies focused on high-performance computing for exposure to this trend.

Market Price: Nvidia (NVDA): $139.34

Buffett Reduces Apple Stake Amid Market Adjustments

Berkshire Hathaway continued trimming its Apple holdings in Q3, reducing its stake by 25%, following a nearly 50% cut in Q2. Despite this, Apple remains Berkshire’s largest holding, suggesting Buffett’s adjustment may be tied to portfolio rebalancing or tax strategies. Berkshire’s cash reserves now stand at a record $325.2 billion, with $34.6 billion in equities sold this quarter, indicating a shift toward liquidity and cautious positioning.

Investment Insight: Berkshire’s stake reduction in Apple could reflect a broader cautious approach. Investors should keep an eye on Berkshire’s moves, as they may indicate broader market sentiment shifts.

Market Price: Apple (AAPL): $222.91

Wall Street Eyes Election, Avoids Big Bets Amid Volatility

With the U.S. presidential election approaching, Wall Street is adopting a cautious stance, refraining from bold moves due to anticipated volatility. The Cboe Volatility Index has climbed as investors hedge against potential post-election market swings. Sectors such as financials, renewable energy, and crypto are seeing defensive options trades, while currency markets brace for fluctuations in the yuan, peso, and euro, anticipating potential shifts in trade policies post-election.

Investment Insight: Rising volatility and caution on Wall Street reflect the uncertain pre-election environment. Investors might consider defensive strategies or hedging options as the election nears.

Bond Traders Pare Back Ahead of Pivotal Week

Bond traders are reducing positions in anticipation of the U.S. election and a likely Federal Reserve rate cut. Treasury yields have been volatile, with traders avoiding significant positions due to the election’s potential impact on fiscal policy. A Republican sweep could push yields higher, while a Democratic win or divided government might bring relief to bondholders. Current volatility in the bond market is the highest seen this year, signaling a cautious outlook.

Investment Insight: Bond market adjustments highlight uncertainty over fiscal policies. Investors should remain attuned to bond market movements as the election outcome becomes clearer.

Asian Markets Rise as China Begins Economic Meeting

Asian shares rose as China began a key economic meeting, sparking optimism for potential fiscal stimulus. Markets in Hong Kong and Shanghai gained on expectations of supportive measures, while South Korea’s Kospi and Australia’s ASX 200 also saw gains. In the U.S., stock futures edged higher following a Friday rally, driven by strong earnings from Amazon and Intel. Meanwhile, oil prices rose over 1% after OPEC+ extended production cuts, with U.S. crude at $70.68 per barrel and Brent at $74.25.

Investment Insight: China’s potential stimulus plans could positively affect global markets, particularly in Asia. However, investors should remain cautious, given the election’s potential impact on international markets.

Market Price:

Brent Crude: $74.25 per barrel

U.S. crude: $70.55 per barrel

Hang Seng Index: HKD 20,561.78

Conclusion

These developments across sectors illustrate the potential for significant shifts based on upcoming events, particularly the U.S. election. Staying informed will be essential for navigating these uncertainties.

Upcoming Dates to Watch

- November 7, 2024: U.S. Federal Reserve interest rate decision.

- November 14, 2024: Eurozone Q3 GDP report release.

- November 13, 2024: U.S. Consumer Price Index (CPI) data release.

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.

Daily Synopsis of the New York market close

Date Issued – 3rd December 2024

Preview

Intel’s CEO departure signals potential strategic shifts, with options like splitting divisions, selling assets, or exploring acquisitions back on the table. HKBN shares surged after China Mobile’s $882 million takeover bid, though regulatory hurdles and rival offers loom. Trump’s vow to block Nippon Steel’s $15 billion bid for U.S. Steel adds uncertainty as the deal undergoes national security review. Super Micro shares jumped 29% after a misconduct probe cleared management, but risks like Nasdaq compliance persist. Meanwhile, Asian markets rallied on optimism around global easing, though Chinese stocks lagged amid economic concerns and a weakening yuan.

Intel CEO Departure Sparks Fresh Deal Talks

The sudden exit of Intel CEO Pat Gelsinger signals a potential turning point for the struggling chipmaker, as its board reconsiders previously rejected strategies. Under Gelsinger, Intel focused on restoring its technological dominance and expanding its foundry business, but with limited success. Now, the company may explore options such as splitting its factory and product divisions, selling underperforming assets like Altera, or revisiting acquisition interest from companies like Qualcomm and Broadcom. New leadership could also consider divesting its stake in Mobileye or pursuing private equity investments to stabilize finances.

Investment Insight: Intel’s leadership shake-up increases the likelihood of structural changes. Investors should monitor potential divestitures or partnerships, as these moves could unlock value, particularly in Intel’s product and foundry businesses. Regulatory hurdles and market volatility remain key risks.

Market price: Intel Corp (INTC): USD 23.93

HKBN Shares Surge as China Mobile Makes $882 Million Bid

HKBN Ltd. shares jumped after China Mobile Ltd. launched a formal takeover bid valuing the Hong Kong broadband provider at HK$6.86 billion ($882 million). The offer, priced at HK$5.23 per share, represents a 41% premium to HKBN’s undisturbed share price. China Mobile has secured commitments from major HKBN shareholders, including Canada Pension Plan Investment Board and TPG, which collectively own 25% of the company. The deal, aimed at expanding China Mobile’s service portfolio in Hong Kong, faces regulatory approval and competition from rival bidder I Squared Capital, which is still negotiating terms for its offer.

Investment Insight: China Mobile’s bid underscores its intent to expand its market position in Hong Kong, offering HKBN shareholders a lucrative premium. Investors should watch for regulatory developments and potential counteroffers from I Squared, which could intensify the bidding war.

Market price: HKBN Ltd (HKG 1310): HKD 5.13

Trump Opposes Nippon Steel’s $15 Billion Bid for U.S. Steel

President-elect Donald Trump reiterated his opposition to Nippon Steel’s $15 billion bid to acquire U.S. Steel, pledging to block the deal after taking office in January. Trump claimed on Truth Social that tax incentives and tariffs would revitalize U.S. Steel without foreign ownership. The deal, strongly opposed by U.S. labor unions, is currently under review by the Committee on Foreign Investment in the United States (CFIUS) for national security risks. Japanese Prime Minister Shigeru Ishiba has urged President Biden to approve the transaction, but the review process could extend into Trump’s presidency, jeopardizing Nippon Steel’s plans.

Investment Insight

The uncertainty surrounding CFIUS approval and Trump’s promise to block the deal create significant risks for Nippon Steel’s bid. Investors should closely monitor regulatory developments and potential delays, which could impact U.S. Steel’s valuation and broader market sentiment.

Market price: Nippon Steel Corp (TYO: 3073): JPY 3073

Super Micro Shares Surge After Key Ruling Clears Management

Super Micro Computer (SMCI) shares surged 29% after a special committee investigating allegations of misconduct found no evidence implicating the company’s management or board. The probe, launched in response to a scathing report by short-seller Hindenburg Research, concluded that concerns raised by Ernst & Young’s resignation as auditor were “unsupported by the facts.” Despite the favorable findings, analysts remain cautious due to regulatory risks, delayed financial filings, and the potential for Nasdaq delisting. The company, which has benefited from AI-driven demand, continues to work toward restoring investor confidence.

Investment Insight

While the special committee’s findings provided relief for investors, lingering uncertainties—such as Nasdaq compliance and the acceptance of findings by new auditors—warrant caution. Investors should monitor regulatory updates and financial clarity before making long-term commitments to the stock.

Market price: Super Micro Computer Inc (SMCI): USD 42.00

Asian Stocks Rally Despite US Tech Curbs on China

Asian markets advanced as investors viewed the Biden administration’s new tech export restrictions on China as less severe than anticipated. Equity benchmarks rose across Japan, Australia, and Hong Kong, led by tech firms, while Chinese stocks lagged, weighed down by a weakening yuan hitting a one-year low. Optimism around robust US economic data and potential global central bank easing lifted sentiment across the region, except for China, where uncertainty over economic policy kept investors cautious. Meanwhile, US futures held steady following record highs for the S&P 500 and gains in the Nasdaq 100.

Investment Insight

The restrained scope of US tech curbs relieved markets, supporting Asian tech stocks. However, China’s underperformance highlights lingering risks from its economic slowdown and geopolitical tensions. Investors should remain selective, focusing on ex-China Asian markets benefiting from resilient US demand and easing monetary conditions.

Conclusion

Intel’s leadership shake-up, China Mobile’s aggressive HKBN bid, and Trump’s opposition to Nippon Steel’s U.S. Steel deal highlight the dynamic intersection of corporate strategy and geopolitical tension shaping markets. Super Micro’s rebound after a misconduct probe offers a cautionary tale on regulatory risks, while Asian markets’ resilience—despite U.S. tech curbs on China—signals investor optimism tied to global easing. Yet, challenges like China’s economic slowdown, regulatory scrutiny, and market volatility remain key themes. As opportunities emerge, staying alert to regulatory shifts, corporate restructuring, and market sentiment will be crucial for navigating an increasingly complex and fast-changing investment landscape.

Upcoming Dates to Watch

- December 6, 2024: US Consumer Sentiment

- December 11, 2024: US CPI

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.

Daily Synopsis of the New York market close

Date Issued – 28th November 2024

Preview

Elon Musk has called for the elimination of the Consumer Financial Protection Bureau (CFPB), describing it as a redundant regulatory body. His stance aligns with his role on Trump’s advisory board for government efficiency, where he aims to reduce federal bureaucracy. Critics argue that the CFPB has targeted fintech firms and crypto entrepreneurs, while the agency defends its efforts to combat consumer deception and safeguard against discriminatory practices. The potential dismantling of the CFPB could ease compliance burdens for startups but might heighten consumer risks. Nissan’s global production dropped 6% in October, and the company faces mounting pressure from President-elect Donald Trump’s proposed 25% tariffs on imports from Mexico and Canada.

Elon Musk Calls for Scrapping the CFPB Amid Regulatory Criticism

Elon Musk, a key adviser to the incoming Trump administration, has called for the elimination of the Consumer Financial Protection Bureau (CFPB), describing it as a redundant regulatory body. In a late-night post on his social media platform, X, Musk wrote, “Delete CFPB. There are too many duplicative regulatory agencies.” His remarks echo recent criticism from venture capitalist Marc Andreessen, who accused the CFPB of stifling innovation and favoring large financial institutions over startups, particularly in fintech and crypto.

Critics argue that the CFPB has targeted fintech firms and crypto entrepreneurs with lawsuits and fines, claiming the agency protects big banks by blocking new entrants. However, the CFPB has defended its actions, citing efforts to combat consumer deception and safeguard against discriminatory practices in financial services.

Musk’s stance aligns with his role on Trump’s advisory board for government efficiency, where he and Vivek Ramaswamy aim to reduce federal bureaucracy. Notably, Musk’s own company, X, has sought licenses to expand into payments — a move that could bring it under CFPB oversight.

Investment Insight: The potential dismantling of the CFPB could ease compliance burdens for fintech and crypto startups, potentially spurring innovation. However, reduced oversight might heighten consumer risks, creating a more volatile regulatory and investment landscape.

Nissan’s Global Production Slumps in October; U.S. Tariff Threat Looms

Nissan’s global production dropped 6% in October, marking its fifth consecutive monthly decline, with steep output falls in China (-15%), the U.S. (-15%), Britain (-23%), and Japan (-4%). Mexico stood out as a bright spot, with production rising 12%, accounting for nearly a quarter of Nissan’s global output. Global sales fell 3%, though U.S. sales grew 13%, driven by the Sentra sedan.

Amid restructuring efforts, including job cuts and capacity reductions, Nissan faces mounting pressure from President-elect Donald Trump’s proposed 25% tariffs on imports from Mexico and Canada. Nissan, which exported 300,000 vehicles from Mexico to the U.S. this year, is closely monitoring the policy’s potential impact.

Investment Insight: Trump’s tariff threats could disrupt supply chains and increase costs for automakers reliant on Mexican exports, including Nissan. Investors should watch for potential shifts in production strategies and the broader impact on U.S.-Mexico trade relations.

Market price: Nissan Motor Co Ltd. (TYO: 721): JPY 374.00

South Korea Cuts Rates Amid Trump Tariff Concerns

The Bank of Korea (BOK) surprised markets with a second consecutive rate cut, lowering its key rate to 3% to counter economic risks posed by President-elect Donald Trump’s proposed tariffs and shifting global trade policies. The BOK also slashed its 2025 growth forecast to 1.9%, citing heightened uncertainties for South Korea’s export-reliant economy.

Trump’s potential 25% tariffs on trade partners, including South Korea, and a rollback of subsidies for foreign firms like Samsung and Hyundai, are expected to pressure exports and investment. The move marks the BOK’s first back-to-back rate cut since 2009, underscoring its urgency to shield the economy from a prolonged slowdown.

Investment Insight: The rate cut may weigh on the Korean won but signals policy prioritization of economic growth over currency stability. Investors should monitor trade policy developments closely as tariff risks could challenge South Korea’s export-heavy sectors and corporate performance.

China’s EV Boom Accelerates Decline in Gasoline Demand

China’s rapid adoption of electric vehicles (EVs) is reshaping its energy landscape, with EVs and hybrids accounting for over half of retail passenger vehicle sales since July. Analysts now expect Chinese gasoline demand to peak as early as next year, with annual declines of 4–5% predicted through 2030. This shift poses a significant challenge for the global oil market, which has relied on China as a key driver of demand growth for decades.

Diesel consumption is also in decline, with UBS projecting annual drops of 3–5% due to the rise of electric and LNG-powered trucks. While uncertainties remain around hybrid vehicle fuel usage and full electrification timelines, Beijing’s decade-long focus on EV subsidies and infrastructure has positioned China as a global leader in transport electrification.

Investment Insight: Plunging gasoline demand in China could weigh on global oil prices and disrupt energy sector investments. Investors should watch for shifts in oil market dynamics, while exploring opportunities in EV supply chains and green energy infrastructure.

Intel’s $7.86 Billion Subsidy Ties Chip Unit Control to U.S. Oversight

Intel’s $7.86 billion subsidy deal with the U.S. government includes stringent restrictions on selling stakes in its chip manufacturing unit, Intel Foundry, if the division spins into a separate entity. Under the agreement, Intel must retain at least 50.1% ownership of Intel Foundry as a private company. If the unit goes public, Intel can only sell up to 35% to a single shareholder without triggering government review.

These conditions are part of a broader $39 billion U.S. effort to boost domestic chip production, which also supports other firms like Taiwan Semiconductor Manufacturing Co. Intel must comply with these terms to sustain its $90 billion in U.S.-based projects across Arizona, New Mexico, Ohio, and Oregon.

Investment Insight: Stringent ownership rules could limit Intel’s flexibility in raising capital for its chip unit, potentially slowing expansion. However, the subsidies reinforce Intel’s role in U.S. chipmaking, offering long-term stability for investors focused on the semiconductor sector.

Market Price: Intel Corp (INTC): USD 23.65

Conclusion

The global economic landscape is shifting rapidly, with regulatory changes, trade tensions, and technological disruptions reshaping key industries. As the U.S. grapples with the potential dismantling of the CFPB and the implementation of tariffs, automakers like Nissan and economies like South Korea face new challenges. Meanwhile, China’s EV boom is accelerating the decline in gasoline demand, potentially disrupting the global oil market. As Intel navigates stringent subsidy conditions, the semiconductor industry faces both opportunities and limitations. Investors must closely monitor these developments to adapt their strategies and capitalize on emerging trends while mitigating risks in an increasingly complex and interconnected world.

Upcoming Dates to Watch

November 28, 2024: Eurozone Economic Sentiment Indicator release

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.

Daily Synopsis of the New York market close

Date Issued – 27th November 2024

Preview

Asian markets were mixed Wednesday as Wall Street hit record highs despite President-elect Trump’s tariff threats. The euro’s slide against the dollar sparks concerns over global market volatility, while OpenAI employees prepare to sell $1.5 billion in shares to SoftBank. Apple lags behind in the 2024 smartphone market rebound, with Android rivals capturing most of the growth. Electric vehicles face headwinds in the U.S. and Europe despite China’s booming EV market, driven by government subsidies and affordable models. Investors should monitor market-specific risks, government policies, and the impact of AI-driven innovations on consumer demand.

Global Markets Update: Asian Shares Mixed Amid Trade Uncertainty

Asian markets were mixed on Wednesday as Wall Street hit record highs despite President-elect Donald Trump’s tariff threats. Japan’s Nikkei fell nearly 1% due to a stronger yen, while South Korea’s Kospi dropped 0.6%, led by Samsung’s management reshuffle and a 3.3% stock decline. In contrast, Chinese markets gained, with Hong Kong’s Hang Seng up 0.5% and the Shanghai Composite rising 0.7%. Australia’s S&P/ASX 200 added 0.5%, while Taiwan and Bangkok markets posted losses.

On Wall Street, the S&P 500 rose 0.6% to a new record of 6,021.63, driven by Big Tech, with Amazon and Microsoft leading gains. However, Trump’s tariff rhetoric sparked concerns over inflation, higher consumer costs, and potential retaliatory moves from key trade partners. Meanwhile, U.S. crude oil edged up to $68.89 per barrel, and the dollar weakened slightly against the yen and euro.

Investment Insight: Market resilience in the face of trade tensions highlights investor confidence in Big Tech and U.S. economic fundamentals. However, Trump’s tariff threats could disrupt supply chains, pressure corporate profits, and exacerbate inflation risks, warranting caution for sectors reliant on global trade.

OpenAI Employees to Sell $1.5 Billion in Shares to SoftBank

OpenAI, the company behind ChatGPT, is allowing employees to sell $1.5 billion worth of shares to Japan’s SoftBank Group in a tender offer reported by CNBC. This follows OpenAI’s recent $6.6 billion funding round, which valued the Microsoft-backed firm at $157 billion. SoftBank, having already invested $500 million in October, is expanding its stake under the leadership of CEO Masayoshi Son. The tender offer, closing this week, offers current and former employees the opportunity to cash out their shares.

Investment Insight: SoftBank’s deepening investment in OpenAI underscores confidence in AI’s growth trajectory. Investors should watch for how this capital infusion supports OpenAI’s scaling efforts and how it impacts SoftBank’s broader AI strategy amid intensifying competition in the sector.

Euro’s Slide Sparks Concerns Over Global Market Volatility

The euro is down 3.8% against the dollar this month, nearing the critical $1 mark, driven by eurozone economic weakness, escalating geopolitical tensions, and proposed U.S. tariffs under President-elect Donald Trump. Analysts warn a further drop could trigger market instability, similar to the August turmoil caused by yen-dollar swings. The euro-dollar pair, the world’s most traded, impacts multinational earnings and global trade dynamics, with spillovers likely to affect currencies in trade-sensitive nations like China and South Korea. Diverging views on the euro’s future underscore market uncertainty, with some forecasting a drop to $0.99 in 2025, while others see a rebound to $1.16.

Investment Insight: Currency volatility poses risks for multinational firms and export-reliant economies. Investors should consider hedging strategies to mitigate exposure to unpredictable euro-dollar swings, while monitoring cross-asset correlations that could amplify market instability.

Apple Lags Behind in 2024 Smartphone Market Rebound

The global smartphone market grew 6.2% in 2024, shipping 1.24 billion units after years of decline, but Apple saw only a marginal 0.4% increase in iPhone shipments, according to IDC. Android-based competitors captured most of the rebound, particularly in China and emerging markets, with affordable devices driving demand. While Apple continues to dominate profits with an average selling price above $1,000, rivals like Xiaomi and Huawei are pushing AI-driven innovations and in-house chip development to gain market share. IDC notes that AI enhancements across brands have yet to spark significant consumer upgrades, as global smartphone shipments remain below pre-pandemic levels.

Investment Insight: Apple’s soft volume growth underscores its reliance on premium pricing rather than unit expansion, while Android rivals capitalize on affordability and regional strategies. Investors should monitor Apple’s efforts to penetrate lower-tier markets and the broader impact of AI-driven features on future upgrade cycles.

Market price: Apple Inc. (AAPL): USD 235.06

Electric Vehicles Face Headwinds in the U.S. and Europe Despite China Boom

While global EV sales are growing, the U.S. and Europe are struggling to match China’s momentum. Concerns over range, charging infrastructure, and high costs are slowing adoption in Western markets, where EV sales remain below climate target levels. China, in contrast, leads with 60% of global EV sales, driven by government subsidies, price cuts, and rising demand for affordable models. U.S. buyers face uncertainty over tax credits as President-elect Trump signals reduced EV support, and Europe grapples with policy rollbacks and slowed growth. Still, automakers remain committed to electrification, betting on long-term market transformation.

Investment Insight: EV adoption disparities signal market-specific risks and opportunities. Watch for Chinese automakers gaining global traction with low-cost models, while Western EV makers face challenges in scaling affordability and infrastructure. Long-term investors should monitor government policies and tax credit shifts that could influence demand trajectories.

Market Price: Tesla Inc. (TSLA): USD 338.23

Conclusion

The global markets face a mix of opportunities and challenges as trade tensions, currency volatility, and technological disruptions shape investor sentiment. While Big Tech drives U.S. market resilience, the euro’s slide and Trump’s tariff threats warrant caution. OpenAI’s share sale to SoftBank highlights the growing interest in AI, even as smartphone makers grapple with varying regional demand. The EV market’s uneven growth across China, the U.S., and Europe underscores the importance of government policies and affordability in driving adoption. As investors navigate these complex dynamics, a strategic approach to risk management and long-term value creation is crucial.

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.

Daily Synopsis of the New York market close

Date Issued – 26th November 2024

Preview

Asian markets slipped on Tuesday amid concerns over potential tariffs on Mexico, Canada, and China, as mentioned by President-elect Donald Trump.

The Nikkei 225, S&P/ASX 200, and Kospi declined, while the Hang Seng remained flat. China is ramping up Brazilian soybean imports due to trade tensions

with the U.S. and favorable prices. Qualcomm has cooled on its potential acquisition of Intel, citing financial and regulatory challenges.

Xiaomi is developing its own mobile processor to reduce dependence on Qualcomm and MediaTek, aligning with Beijing’s push for self-reliance in technology.

Best Buy is eyeing AI products for growth and expects to report flat Q3 earnings, with AI-enabled devices potentially offsetting sluggish appliance sales.

Asian Markets Slip Amid Tariff Concerns

Asian shares mostly fell on Tuesday following President-elect Donald Trump’s comments on imposing tariffs on Mexico, Canada, and China.

Japan’s Nikkei 225 dropped 0.9%, Australia’s S&P/ASX 200 slid 0.7%, and South Korea’s Kospi declined 0.6%. Meanwhile, Hong Kong’s Hang Seng was flat,

and the Shanghai Composite edged up 0.1%. Concerns over trade policy overshadowed Wall Street’s gains on Monday, where the S&P 500 rose 0.3%,

and the Dow hit a record high. U.S. Treasury yields eased after Trump floated hedge fund manager Scott Bessent as a potential Treasury Secretary,

fueling hopes of deficit control.

Investment Insight: Heightened trade tensions could weigh on Asian markets while lower U.S. Treasury yields may benefit equities.

Investors should monitor inflation data and Fed rate policy for near-term market direction.

China Ramps Up Brazilian Soybean Imports Amid Trade Tensions

Chinese buyers are securing record volumes of Brazilian soybeans, taking advantage of low prices and abundant supply from Brazil’s expected largest-ever harvest.

Concerns over renewed trade tensions with the U.S., as President-elect Donald Trump threatens new tariffs on Chinese goods, have pushed Chinese crushers to stock up early,

even during Brazil’s off-season. Brazilian soybeans are priced $22 per ton cheaper than U.S. beans for March deliveries, according to Commodity3 data.

While the U.S. still accounts for some Chinese purchases, sales remain at their lowest for this time of year since 2018, reflecting uncertainty over trade policies.

Investment Insight: China’s pivot to Brazilian soybeans signals potential headwinds for U.S. agriculture. Investors in commodities and agribusiness should

watch for tariff developments and shifts in global supply chains.

Qualcomm Cools on Intel Takeover Amid Complexities

Qualcomm has reportedly backed away from pursuing an acquisition of Intel, citing the deal’s financial and regulatory challenges, including Intel’s $50 billion debt and its

loss-making manufacturing unit. The potential takeover, which could have been one of the largest tech deals ever, faced antitrust hurdles and operational risks. Qualcomm may

still explore acquiring parts of Intel or revisit the idea in the future. Both firms are navigating shifting industry dynamics, with Qualcomm targeting new markets and Intel

striving to regain its footing in the AI-driven chip race.

Investment Insight: The cooled takeover reflects the growing complexity of mega-deals in the semiconductor sector. Investors should focus on Qualcomm’s organic

growth initiatives and Intel’s restructuring efforts for long-term opportunities.

Market price: QCOM: USD 158.82

Xiaomi Prepares In-House Chip, Targeting Qualcomm and MediaTek

Xiaomi is developing its own mobile processor, with mass production slated for 2025, aiming to reduce dependence on Qualcomm and MediaTek. This move aligns with Beijing’s

push for self-reliance in technology amid U.S.-China tensions. While Apple and Google have succeeded in designing proprietary chips, other firms like Oppo and Nvidia have

struggled, highlighting the challenges Xiaomi faces. In-house chipmaking could boost Xiaomi’s smartphone competitiveness and support its broader ambitions in connected tech,

including electric vehicles, as the company ramps up R&D investments to $4.1 billion in 2025.

Investment Insight: Xiaomi’s chip strategy could disrupt the supply chain dynamics for Qualcomm and MediaTek. Investors should watch for advancements in Xiaomi’s

semiconductor capabilities and its potential to reshape the Android device market.

Market price: Xiaomi: HKD 27.25

Best Buy Eyes AI Products for Growth Amid Stabilizing Demand

Best Buy is set to report its Q3 results, with Wall Street expecting flat adjusted earnings of $1.29 per share on $9.63 billion in revenue, slightly below last year. Same-store

sales are forecasted to dip nearly 1%, an improvement from a 7.3% decline a year ago. Appliance sales are expected to drag, while computing and mobile phones may see gains,

supported by demand for AI-enabled products like Copilot+ PCs. Best Buy remains optimistic about AI as a growth driver, with exclusivity deals on 40% of new AI PCs and a broader

rollout anticipated in 2025.

Investment Insight: Best Buy’s focus on AI products positions it to capitalize on tech-driven consumer trends. Investors should monitor its ability to offset

sluggish appliance sales with demand for emerging AI-enabled devices.

Market price: Best Buy Co (BBY): USD 93.03

Conclusion

The newsletter highlights the complex interplay of geopolitical tensions, technological advancements, and shifting consumer trends in shaping the global market landscape. As

trade tensions persist, companies are navigating supply chain disruptions and exploring new strategies for growth. The semiconductor industry faces challenges in mega-deals,

while the rise of AI presents opportunities for firms to differentiate and capture emerging demand. Investors should closely monitor these developments, focusing on companies’

ability to adapt and innovate in an increasingly dynamic and competitive environment. By staying attuned to these key trends, investors can position themselves to capitalize on

the long-term opportunities that arise.

Upcoming Dates to Watch:

November 28, 2024: Eurozone Economic Sentiment Indicator release

Bond Market Stabilizes as Bessent’s Treasury Nomination Calms Markets

The U.S. bond market is finding its footing after a two-month selloff, with investors stepping in at 4.5% yields.

Treasury yields, which peaked on Nov. 15, have since dipped to 4.36% following Scott Bessent’s nomination as U.S. Treasury Secretary.

Bessent, a fiscal hawk, has pledged to cut the deficit to 3% of GDP through spending cuts and economic growth, though skeptics question

the feasibility of reducing essential expenditures like Medicare and defense. His commitment to a strong dollar contrasts with Trump’s

past devaluation rhetoric, and his fiscally disciplined stance has eased market concerns, driving a 6-basis-point drop in 10-year yields.

Despite the recent rally, uncertainty over Trump’s fiscal policies, inflation, and potential tariffs—some as high as 60% on Chinese goods—keeps

volatility elevated. While some strategists see 4.25%-4.5% as fair value for 10-year Treasuries, others caution that yields could rise further

if aggressive fiscal stimulus boosts inflation. Traders are now awaiting the Fed’s preferred inflation gauge, the PCE price index, for additional clarity.

Investment Insight: Treasuries at 4.5% yields present attractive returns, but volatility may persist amid fiscal policy uncertainty.

Bessent’s nomination signals fiscal discipline, which could support bonds but pose risks for equities if aggressive deficit reduction slows growth.

Investors should monitor tariff developments, Fed-ECB rate divergence, and inflation data for guidance.

US10Y Yield: 4.328%

Meituan, Chow Tai Fook Earnings to Gauge China’s Consumer Sentiment

Earnings from Meituan and Chow Tai Fook Jewellery this week are set to provide insights into China’s struggling consumer market, weighed down

by a sluggish economic recovery, property woes, and job instability. Despite these headwinds, October retail sales saw their fastest growth in

eight months, supported by government stimulus efforts that have yet to meaningfully boost household incomes.

Meituan is expected to defy the broader slowdown, with Morgan Stanley predicting strong growth driven by consumption voucher programs and

policy support for platform economies. In contrast, Chow Tai Fook’s first-half earnings are likely to reflect weak retail sentiment and high gold prices,

with revenue projected to decline up to 22%.

Investment Insight: Meituan’s resilience highlights opportunities in platform-driven sectors benefiting from policy tailwinds,

while Chow Tai Fook underscores challenges in discretionary spending. Cautious positioning in China’s consumer sector is warranted until income growth stabilizes.

Market price: Meituan (3690.hk): HKD 161.00

Rio Tinto-Backed Lithium Startup Nears $19M Fundraising Amid Market Struggles

ElectraLith, a Rio Tinto-backed lithium technology startup, is set to close an oversubscribed A$29 million ($19 million) funding round despite weak global lithium

and venture capital markets. The company’s innovative direct lithium extraction (DLE) technology uses no water or chemicals, making it ideal for arid regions like

Chile’s Atacama Desert. ElectraLith plans to use the funds to construct its first pilot plant at Rio Tinto’s Rincon operations in Argentina within a year, followed

by two additional pilot plants. The DLE-R process, which filters brine to produce lithium hydroxide at half the cost of competitors, could revolutionize the lithium

industry by drastically shortening production timelines and addressing water scarcity challenges.

Investment Insight: ElectraLith’s cost-efficient and sustainable DLE technology positions it favorably in the growing lithium market,

which could surpass $10 billion annually within a decade. Investors should watch how the startup scales its technology and competes in the evolving EV battery supply chain.

Market Price: Rio Tinto: USD 62.50

Conclusion:

The global investment landscape is rapidly evolving, shaped by geopolitical shifts, technological innovation, and changing consumer trends.

As the U.S. navigates a political transition and China faces structural challenges, Southeast Asia grapples with the potential fallout from

Trump’s protectionist policies. Investors must remain vigilant, monitoring developments in key sectors like cryptocurrencies, bonds, consumer

goods, lithium, semiconductors, and EVs. Diversification and adaptability will be crucial in mitigating risks and seizing opportunities amidst

uncertainty. The coming weeks will provide further clarity on the future of these critical industries and the economies they support, as the world

braces for a new era of change.

Upcoming Dates to Watch:

November 28, 2024: Eurozone Economic Sentiment Indicator release

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.