Daily Synopsis of the New York market close

Date Issued – 25th November 2024

Preview

Howard Lutnick, Trump’s Commerce Secretary nominee, is in talks with Tether for a $2 billion bitcoin lending project that could scale to tens of billions. China’s dairy boom is slowing, with revenue for top producers dropping up to 13% in H1 2024 amid overcapacity and demographic shifts. The U.S. bond market is stabilizing after Scott Bessent’s Treasury nomination, but volatility persists over fiscal policy uncertainty. Meituan and Chow Tai Fook’s earnings will gauge China’s struggling consumer market. ElectraLith, a Rio Tinto-backed lithium startup, nears a $19 million fundraise for its innovative, cost-efficient extraction technology despite weak markets. Trump’s anticipated tariffs threaten Southeast Asia’s trade growth, potentially impacting semiconductors, EVs, and clean energy sectors.

Trump Nominee Lutnick in Talks with Tether for $2B Bitcoin Lending Push

Howard Lutnick, U.S. President-elect Donald Trump’s pick for Commerce Secretary, is reportedly eyeing a $2 billion bitcoin-backed

lending project in collaboration with Tether, the issuer of the largest stablecoin. Lutnick’s firm, Cantor Fitzgerald, is in discussions

to leverage Tether’s financial support for the initiative, which could scale to tens of billions of dollars. Tether, which already works

closely with Cantor to manage billions in U.S. Treasuries backing its stablecoin, confirmed its interest in exploring new investment

opportunities. This move underscores Lutnick’s advocacy for cryptocurrency adoption as he prepares to lead the Commerce Department.

Investment Insight: A partnership between a major financial firm and Tether signals growing institutional interest

in crypto-backed lending, but regulatory scrutiny and market volatility remain key risks for investors.

Trump’s Tariff Policies Threaten Southeast Asia’s Trade Growth

Donald Trump’s anticipated return to the White House raises concerns for Southeast Asian economies like Malaysia, Thailand, and Vietnam,

which previously benefited from his trade war with China. During Trump’s first term, Chinese firms relocated supply chains to the region,

boosting investment and jobs. However, the new administration’s focus on curbing “third-country workarounds” could result in tariffs as

high as 20% on imports from nations with large trade surpluses, particularly in strategic sectors like semiconductors and electric vehicles.

Steve Alain Lawrence, CIO of Balfour Capital, suggests that affected Asian nations could retaliate with tariffs on U.S. goods or impose

non-tariff barriers, further complicating trade dynamics. Analysts warn of potential export declines, retreating foreign investment, and

strained manufacturing supply chains, while regional governments explore free trade agreements and alliances to mitigate risks.

Investment Insight: Southeast Asia’s trade-reliant economies may face headwinds as Trump’s protectionist policies target

supply chain reconfigurations. Investors should monitor impacts on semiconductors, EVs, and clean energy sectors while considering

diversification into resilient industries and regions.

China’s Dairy Boom Nears Its End, S&P Warns

China’s decades-long dairy expansion is slowing, with revenue for the top three producers dropping up to 13% in the first half of 2024,

according to S&P Global Ratings. A shrinking population and sluggish economy are expected to halve annual growth in dairy sales volumes

to 2%-3% over the next 20 years. Overcapacity and a 40% rise in domestic milk production over the past decade have further exacerbated

pressure on the sector. While the government considers limiting EU imports to ease strain on farmers, S&P predicts the aging population

may stabilize demand in 10 to 15 years.

Investment Insight: China’s dairy industry faces structural challenges, including demographic shifts and overproduction.

Investors should anticipate volatile earnings and focus on companies adapting to long-term trends like aging-related consumption.

Bond Market Stabilizes as Bessent’s Treasury Nomination Calms Markets

The U.S. bond market is finding its footing after a two-month selloff, with investors stepping in at 4.5% yields.

Treasury yields, which peaked on Nov. 15, have since dipped to 4.36% following Scott Bessent’s nomination as U.S. Treasury Secretary.

Bessent, a fiscal hawk, has pledged to cut the deficit to 3% of GDP through spending cuts and economic growth, though skeptics question

the feasibility of reducing essential expenditures like Medicare and defense. His commitment to a strong dollar contrasts with Trump’s

past devaluation rhetoric, and his fiscally disciplined stance has eased market concerns, driving a 6-basis-point drop in 10-year yields.

Despite the recent rally, uncertainty over Trump’s fiscal policies, inflation, and potential tariffs—some as high as 60% on Chinese goods—keeps

volatility elevated. While some strategists see 4.25%-4.5% as fair value for 10-year Treasuries, others caution that yields could rise further

if aggressive fiscal stimulus boosts inflation. Traders are now awaiting the Fed’s preferred inflation gauge, the PCE price index, for additional clarity.

Investment Insight: Treasuries at 4.5% yields present attractive returns, but volatility may persist amid fiscal policy uncertainty.

Bessent’s nomination signals fiscal discipline, which could support bonds but pose risks for equities if aggressive deficit reduction slows growth.

Investors should monitor tariff developments, Fed-ECB rate divergence, and inflation data for guidance.

US10Y Yield: 4.328%

Meituan, Chow Tai Fook Earnings to Gauge China’s Consumer Sentiment

Earnings from Meituan and Chow Tai Fook Jewellery this week are set to provide insights into China’s struggling consumer market, weighed down

by a sluggish economic recovery, property woes, and job instability. Despite these headwinds, October retail sales saw their fastest growth in

eight months, supported by government stimulus efforts that have yet to meaningfully boost household incomes.

Meituan is expected to defy the broader slowdown, with Morgan Stanley predicting strong growth driven by consumption voucher programs and

policy support for platform economies. In contrast, Chow Tai Fook’s first-half earnings are likely to reflect weak retail sentiment and high gold prices,

with revenue projected to decline up to 22%.

Investment Insight: Meituan’s resilience highlights opportunities in platform-driven sectors benefiting from policy tailwinds,

while Chow Tai Fook underscores challenges in discretionary spending. Cautious positioning in China’s consumer sector is warranted until income growth stabilizes.

Market price: Meituan (3690.hk): HKD 161.00

Rio Tinto-Backed Lithium Startup Nears $19M Fundraising Amid Market Struggles

ElectraLith, a Rio Tinto-backed lithium technology startup, is set to close an oversubscribed A$29 million ($19 million) funding round despite weak global lithium

and venture capital markets. The company’s innovative direct lithium extraction (DLE) technology uses no water or chemicals, making it ideal for arid regions like

Chile’s Atacama Desert. ElectraLith plans to use the funds to construct its first pilot plant at Rio Tinto’s Rincon operations in Argentina within a year, followed

by two additional pilot plants. The DLE-R process, which filters brine to produce lithium hydroxide at half the cost of competitors, could revolutionize the lithium

industry by drastically shortening production timelines and addressing water scarcity challenges.

Investment Insight: ElectraLith’s cost-efficient and sustainable DLE technology positions it favorably in the growing lithium market,

which could surpass $10 billion annually within a decade. Investors should watch how the startup scales its technology and competes in the evolving EV battery supply chain.

Market Price: Rio Tinto: USD 62.50

Conclusion:

The global investment landscape is rapidly evolving, shaped by geopolitical shifts, technological innovation, and changing consumer trends.

As the U.S. navigates a political transition and China faces structural challenges, Southeast Asia grapples with the potential fallout from

Trump’s protectionist policies. Investors must remain vigilant, monitoring developments in key sectors like cryptocurrencies, bonds, consumer

goods, lithium, semiconductors, and EVs. Diversification and adaptability will be crucial in mitigating risks and seizing opportunities amidst

uncertainty. The coming weeks will provide further clarity on the future of these critical industries and the economies they support, as the world

braces for a new era of change.

Upcoming Dates to Watch:

November 28, 2024: Eurozone Economic Sentiment Indicator release

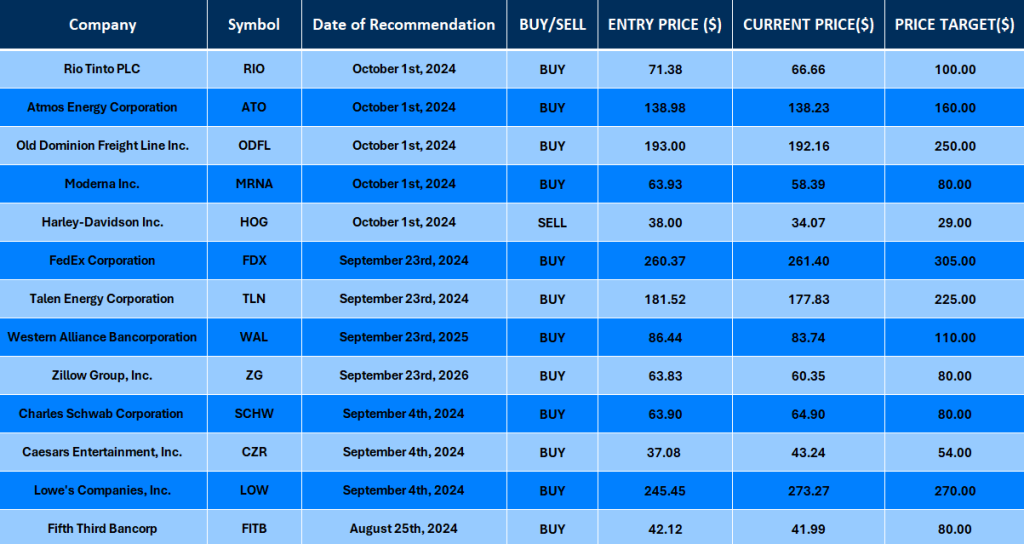

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.

Daily Synopsis of the New York market close

Date Issued – 22nd November 2024

Asian Stocks Rise on Nvidia Earnings and Bitcoin Rally

Asian stocks tracked Wall Street gains on Friday, buoyed by Nvidia’s strong earnings and a surge in bitcoin prices.

Key regional benchmarks, including Japan’s Nikkei 225 (+1%) and South Korea’s Kospi (+1.2%), advanced, while Hong Kong’s Hang Seng

and China’s Shanghai Composite saw slight declines. Nvidia’s robust demand for AI chips propelled U.S. markets, with the S&P 500

rising 0.5%, while bitcoin briefly surpassed $99,000 before retreating. Crypto markets rallied further on news of SEC Chair

Gary Gensler’s pending resignation, fueling optimism for a lighter regulatory stance.

Investment Insight: Tech-driven earnings and crypto momentum are lifting markets, but volatility remains high.

Investors should balance exposure to high-growth sectors with defensive assets, as geopolitical and inflation risks persist.

Adani Group Faces Downgrade Amid U.S. Indictment Fallout

S&P Global Ratings has downgraded its outlook on three Adani Group entities from stable to negative, citing concerns over funding

access following U.S. bribery charges against founder Gautam Adani. The indictment accuses Adani and seven others of a $265 million

scheme to bribe Indian officials for power-supply deals. Adani Group has dismissed the allegations as baseless and pledged legal

recourse. S&P warned that the charges could erode investor confidence, raise funding costs, and disrupt the group’s ambitious growth

plans, given its reliance on equity and debt markets. Adani Group stocks and bonds extended losses for a second consecutive session.

Investment Insight: The indictment highlights reputational and credit risks in emerging markets.

Investors should monitor funding access and refinancing challenges for highly leveraged firms like Adani Group, as these could signal

broader market vulnerabilities.

Market price: Adani Enterprises Ltd: INR 2264.65

Market Update

BOJ Likely to Raise Rates in December as Yen Weakens, Trump Victory Fuels Inflation Expectations

A Reuters poll suggests the Bank of Japan (BOJ) will hike interest rates at its December meeting, with 56% of economists

predicting a raise to 0.50% amid yen depreciation and a strengthening economy. The poll also notes that Donald Trump’s election

victory could push the BOJ to act further, as inflationary policies in the U.S. might stoke global inflationary pressures. BOJ

Governor Kazuo Ueda highlighted the risks of keeping rates too low as Japan moves toward sustained wage-driven inflation. By

March 2025, 90% of analysts anticipate rates will reach 0.50%, with some forecasting further hikes to 0.75% in early 2025.

Investment Insight: Japan’s tightening monetary stance signals a shift from ultra-loose policies, with

potential implications for yen strength and export competitiveness. Investors should watch for opportunities in Japanese financials

and exporters sensitive to currency movements.

Gold Soars as War Risks Intensify, Euro Slumps

Gold surged 4.5% this week, its largest weekly gain in eight months, as geopolitical tensions escalated. Russia fired a hypersonic

missile at Ukraine and lowered its nuclear weapons threshold, triggering safe-haven demand. Meanwhile, shares of Hunan Gold Corp.

surged by their 10% limit for two consecutive days following the discovery of significant gold resources in China’s Hunan province.

The find, estimated at 300 tons with deeper potential reserves, highlights China’s role as the world’s largest gold consumer.

Elsewhere, the euro fell to a 13-month low amid Europe’s economic and political challenges, Brent crude climbed 4.5% on supply concerns,

and Bitcoin hovered near $100,000, adding to market volatility.

Investment Insight: Heightened geopolitical risks and new discoveries are boosting gold’s appeal.

Investors should consider gold mining stocks and ETFs as a hedge against uncertainty, while remaining cautious on euro-denominated

assets amid Europe’s fragility.

Three BofA India Bankers Exit Amid Stock Offering Probe

Three senior Bank of America dealmakers in India, including Debasish Purohit, co-head of investment banking, have left amid an

internal probe into allegations of misconduct tied to stock offerings. Transactions under scrutiny include a $178 million share

sale by Aditya Birla Sun Life Asset Management in March. Indian regulators began investigating the matter in September, raising

questions about compliance practices. Bank of America has yet to comment or name replacements for the departing bankers.

Investment Insight: The probe underscores regulatory risks in emerging markets. Investors should monitor

compliance issues tied to capital markets activity, particularly in regions with heightened regulatory scrutiny, as such risks could

impact financial institutions’ reputations and operations.

Conclusion:

This week’s market developments underscore the complex interplay of geopolitical risks, regulatory challenges, and shifting

economic landscapes. As investors navigate these uncertainties, a balanced approach that combines growth-oriented investments

with defensive strategies appears prudent. Opportunities may arise in sectors like technology and gold mining, while caution

is warranted in regions facing heightened regulatory scrutiny or political instability. Ultimately, staying attuned to global

events, monitoring key risk factors, and maintaining a diversified portfolio will be essential for weathering the volatility

ahead and positioning for long-term success in an increasingly dynamic investment environment.

Upcoming Dates to Watch:

November 22, 2024: Japan National CPI release

November 28, 2024: Eurozone Economic Sentiment Indicator release

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.

Daily Synopsis of the New York market close

Date Issued – 21st November 2024

China’s Role in Preventing Nuclear Escalation, Macron Highlights at G20

At the G20 summit in Rio de Janeiro, French President Emmanuel Macron urged China to play a decisive role in averting nuclear escalation as tensions rise globally. Speaking at the summit, Macron called on Chinese President Xi Jinping to pressure Russian President Vladimir Putin to end the war in Ukraine. This follows Ukraine’s first use of U.S.-made ATACMS missiles to strike deep into Russian territory, prompting Putin to lower Russia’s nuclear strike threshold. Macron also pointed to North Korea’s involvement in the conflict, which raises the stakes for China to advocate for de-escalation.

Putin’s updated nuclear doctrine now considers attacks using advanced Western weapons, like ATACMS, as potential triggers for nuclear retaliation, heightening concerns over the conflict’s trajectory. Macron, meanwhile, announced plans to host U.S. President-elect Donald Trump and billionaire Elon Musk at an AI summit in France in February.

Investment Insight: Rising geopolitical tensions and nuclear risks could increase market volatility, particularly in commodities and defense sectors. Investors should closely monitor China’s diplomatic role and its potential impact on trade and global supply chains.

Nvidia Surpasses Expectations, Fuels the “Age of AI”

Nvidia reported Q3 earnings that exceeded Wall Street projections, driven by surging demand for its AI chips. The company posted earnings per share (EPS) of $0.81 on $35.1 billion in revenue, outperforming analyst expectations of $0.74 EPS and $33.2 billion in revenue. Nvidia’s Data Center segment, accounting for the bulk of its income, saw a 112% year-over-year jump to $30.8 billion. Gaming revenue also beat forecasts, reaching $3.3 billion.

CEO Jensen Huang declared the “age of AI is in full steam,” as the firm anticipates Q4 revenue of $37.5 billion, slightly ahead of expectations. However, Nvidia faces looming challenges, including potential global tariffs under President-elect Donald Trump, which could impact its Taiwan-manufactured chips and squeeze profit margins.

Investment Insight: Nvidia’s dominance in AI positions it as a long-term leader, but geopolitical risks and supply constraints could pressure margins. Investors should watch U.S.-China trade policies and global chip supply trends closely.

Market price: Nvidia Corp (NVDA): USD 145.89

Adani Group Loses $30 Billion in Market Value After U.S. Indictments

Shares of India’s Adani Group plunged on Thursday, wiping out $28 billion in market value following U.S. criminal and civil charges against Chairman Gautam Adani and top executives. The indictments allege $265 million in bribes to Indian officials for contracts tied to solar power projects. Flagship Adani Enterprises dropped 23%, with other group companies like Adani Ports, Adani Green, and Adani Power falling between 20% and 90%.

The fallout extends beyond equities, as Adani’s dollar bonds also saw sharp declines, marking the biggest drop since the group faced allegations of stock manipulation by Hindenburg Research in early 2023. Analysts warn this could damage Adani’s credibility, deter investors, and raise borrowing costs.

Investment Insight: Adani’s legal troubles may undermine investor confidence in emerging-market conglomerates with high debt exposure. Watch for increased risk premiums on Indian corporate bonds and ripple effects on global ESG-focused investments.

Market price: Adani Enterprises Ltd: INR 2298.45

Market Insights

Justice Department Pushes for Google Chrome Sale to Break Monopoly

The Justice Department and several U.S. states have proposed major structural changes to Alphabet Inc.’s Google, including the forced sale of its Chrome browser, to curb the tech giant’s dominance in online search. The move follows a landmark antitrust ruling that Google illegally monopolized search and search advertising. Regulators argue Chrome reinforces Google’s dominance by serving as a gateway to the internet for many users.

Proposals also include licensing Google’s search data to rivals, prohibiting exclusive deals with device makers, and offering users a “choice screen” for selecting search engines. The government further seeks to curtail Google’s AI-related investments to prevent it from monopolizing emerging search technologies. A final ruling is expected after hearings in 2024.

Investment Insight: A forced divestiture of Chrome could reshape the competitive landscape for browsers and search engines, opening opportunities for rivals like Microsoft and AI-driven platforms. Investors should monitor regulatory risks for big tech stocks and potential shifts in the digital advertising market.

Market Price: Alphabet Inc (GOOG): USD 177.33

Trump’s Trade and Commerce Nominee Draws Attention for China Ties

President-elect Donald Trump’s nomination of Howard Lutnick to lead U.S. trade and commerce agencies has sparked debate over his extensive financial ties to China. Lutnick’s firms, including BGC Group and Cantor Fitzgerald, have partnered with Chinese state-owned entities and facilitated Chinese companies’ access to U.S. capital markets, such as underwriting IPOs. Supporters highlight Lutnick’s deep experience in global finance and trade as valuable assets in navigating complex U.S.-China economic relations.

Critics, however, point to potential conflicts of interest stemming from BGC’s joint venture with China Credit Trust, a state-owned firm, and Cantor Fitzgerald’s past deals with Chinese firms. Lawmakers and ethics experts have raised concerns about his impartiality in making key decisions on tariffs, export controls, and trade policy. Despite this, proponents argue that Lutnick’s financial expertise and global network could bolster U.S. competitiveness in trade negotiations.

Investment Insight: Lutnick’s nomination could lead to a pragmatic approach to U.S.-China trade, balancing tougher enforcement with opportunities to strengthen U.S. business interests abroad. Investors should monitor policy shifts in tariffs, export controls, and capital market access, particularly in tech, finance, and manufacturing sectors.

Kioxia Aims for $4.8 Billion IPO in Tokyo to Boost Memory Sector Presence

Bain Capital-backed Kioxia Holdings plans to list on the Tokyo Stock Exchange in mid-December with a valuation of ¥750 billion ($4.8 billion). The IPO, benefiting from a faster approval process, is set to provide much-needed funds for the NAND memory maker to expand capacity and close the gap with industry leader Samsung Electronics. The listing comes after years of delays, during which Kioxia weathered six consecutive quarters of operating losses amid a prolonged slump in NAND prices.

The IPO is expected to help Kioxia capitalize on a recovery in chip prices, though its reliance on a single memory type leaves it more exposed to market volatility than rivals like Samsung and SK Hynix. Bain Capital holds a 56% stake in Kioxia, with Toshiba and Hoya owning 41% and 3%, respectively.

Investment Insight: Kioxia’s IPO reflects renewed optimism in the memory chip market. A successful debut could signal a recovery for the sector, but investors should weigh risks tied to Kioxia’s narrow product focus and competition from dominant players like Samsung.

Flour Millers Face Wheat Supply Crunch as Farmers Hold Out for Better Prices

Flour millers across Asia and the Middle East are grappling with tightening wheat supplies as farmers in key exporting nations, including the U.S., Australia, and Black Sea regions, hold back grain, hoping for higher prices. With global wheat prices near four-year lows and projected stockpiles at a nine-year low, millers are reducing their inventories, leaving them exposed to potential price surges. Current stock coverage is down to 45 days in some regions, far below the typical three-to-four-month buffer.

Despite strong harvests in Australia and Argentina, low farmer sales and high interest rates are limiting millers’ ability to replenish stocks. Meanwhile, Russia, the world’s largest wheat exporter, faces supply constraints with an upcoming grain export quota expected to significantly reduce available stock.

Investment Insight: Global wheat markets are vulnerable to weather risks and geopolitical disruptions, which could trigger sharp price rallies. Investors in agricultural commodities should monitor supply bottlenecks and stockpile trends, particularly in the U.S., Black Sea, and Australia.

Conclusion

This week’s newsletter highlights the complex geopolitical landscape and its potential impact on global markets. From rising nuclear tensions to high-stakes trade nominations and supply chain disruptions, investors must navigate a world of uncertainty. However, amidst these challenges lie opportunities in sectors such as AI, memory chips, and agricultural commodities. To succeed, investors should closely monitor policy shifts, regulatory risks, and market trends while maintaining a diversified portfolio. By staying informed and adaptable, savvy investors can position themselves to weather volatility and capitalize on the unique opportunities presented by these turbulent times.

Upcoming Dates to Watch

- November 22, 2024: Japan National CPI release

- November 28, 2024: Eurozone Economic Sentiment Indicator release

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.

Daily Synopsis of the New York market close

Date Issued – 20th November 2024

Stocks Drift as Investors Await Nvidia Earnings

Asian stocks dipped and European futures pointed to a muted session as traders awaited Nvidia’s earnings report. The MSCI Asia Pacific Index fell 0.5%, while Euro Stoxx 50 futures rose 0.4%. US stock futures also inched higher after Wall Street closed with modest gains on Tuesday, despite escalating tensions in Ukraine. Nvidia, which has been a key driver of market sentiment due to its leadership in AI hardware, surged 4.9% ahead of its earnings release, with investors expecting another strong quarter.

In other developments, Tokyo Gas shares soared after Elliott Investment Management disclosed a major stake, and Seven & I shares rallied on rumors of a potential privatization deal. Meanwhile, US 10-year Treasury yields remained steady, and Bitcoin hit another record high, buoyed by the growing embrace of digital assets under President-elect Donald Trump. Gold also continued its rise amid geopolitical tensions.

Investment Insight: Nvidia’s earnings report could significantly influence tech sector momentum heading into year-end. A strong performance may sustain the current rally, but any disappointment could trigger a broader market pullback. Investors should monitor Nvidia’s results closely, as they will likely set the tone for the final weeks of 2024.

Market price: NVDA: $147.01

Hong Kong Property Tycoons Back IPO Market Revival

Hong Kong’s property magnates are returning to the IPO scene, fueling optimism for a revival in the city’s listing market. Billionaire Robert Ng’s Sino Land and a vehicle tied to Henry Cheng’s New World Development have invested heavily in the $793 million IPO of SF Holding, China’s leading courier service. This marks the first time in years that local tycoons have participated as cornerstone investors, signaling renewed confidence in Hong Kong’s financial markets. After a slow 2023, IPO fundraising has surged 92% this year to $9.1 billion, with SF Holding eyeing one of the largest offerings of 2024.

Investment Insight: The involvement of Hong Kong’s property tycoons in IPOs signals confidence in the city’s market recovery. Investors should watch SF Holding’s performance closely, as it may set the tone for upcoming listings and broader sentiment towards Chinese issuers.

US LNG Exports to China Surge, But Trade Tensions Loom

US liquefied natural gas (LNG) exports to China have soared this year, with imports rising 63% in the first 10 months of 2024 compared to 2023. This jump has moved the US to fifth place among China’s LNG suppliers. However, the surge could be short-lived as the incoming Trump administration may reignite trade tensions with Beijing. If a 60% tariff on Chinese goods is imposed, retaliatory measures could target US gas exports, echoing the last trade war when US LNG shipments to China plummeted in 2019.

Investment Insight: While US LNG exports to China are booming, geopolitical risks could disrupt future growth. Investors in US energy and LNG sectors should remain cautious, as a renewed trade war could significantly impact demand from one of the world’s largest gas importers.

Volkswagen Faces Rising Labor Costs Amid Union Negotiations

Volkswagen is grappling with high labor costs as it prepares for wage negotiations with unions representing 120,000 German workers. Data shows VW spends a higher percentage of revenue on labor than competitors like BMW, Mercedes-Benz, and Stellantis. While VW’s global labor cost ratio fell to 15.4% in 2023, it still exceeds the 9.5%-11% seen at rival firms. With unions demanding a 7% pay hike and VW proposing a 10% cut, tensions are rising. High wages, compounded by Germany’s costly labor market, are straining the company’s competitiveness, particularly as cheaper Chinese models flood the market.

Investment Insight: Volkswagen’s rising labor costs, especially in Germany, could pressure its margins and profitability. Investors should closely monitor the outcome of wage negotiations, as significant cost reductions may be necessary to maintain market leadership and compete with lower-cost rivals.

Market Price: Volkswagen Group (VOW3): EUR 82.98

Hon Hai Secures $1.1 Billion Loan Amid AI Server Demand Surge

Taiwan’s Hon Hai Precision Industry, better known as Foxconn, has secured a $1.1 billion three-year loan from 17 banks, including both local and international lenders. The funds, designated for general corporate purposes, come as the company rides a wave of booming demand for AI servers. Foxconn, which partners with Nvidia, is forecasting continued growth in its AI server business into 2025, with cloud products expected to rival its mobile phone sales. The company is also constructing the world’s largest Nvidia server assembly plant in Mexico.

Investment Insight: Hon Hai’s significant investment in AI infrastructure underscores the sector’s growth potential. Investors should monitor the AI server market closely, as it could become a key revenue driver for both Foxconn and Nvidia, potentially sustaining their stock momentum into 2025.

Market price: Hon Hai 2317.TW: TWD 206.00

Conclusion

As 2024 draws to a close, investors are keeping a close eye on key developments across various sectors. Nvidia’s earnings report will likely set the tone for the tech sector, while Hong Kong’s IPO market revival hinges on the performance of SF Holding. Geopolitical risks threaten to disrupt US LNG exports to China, and the AI server market’s growth potential is underscored by Hon Hai’s significant investments. Meanwhile, Volkswagen’s rising labor costs in Germany could strain its competitiveness and profitability. As the year concludes, these crucial factors will shape investment strategies and market sentiment heading into 2025.

Upcoming Dates to Watch

- November 20, 2024: U.S. Federal Open Market Committee (FOMC) meeting minutes

- November 22, 2024: Japan National CPI release

- November 28, 2024: Eurozone Economic Sentiment Indicator release

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.

Daily Synopsis of the New York market close

Date Issued – 19th November 2024

Goldman Sachs Joins Morgan Stanley in S&P 500 Target of 6,500 by 2025

Goldman Sachs has set a year-end 2025 target of 6,500 for the S&P 500, projecting a 10.3% increase from its recent close of 5,893.62. This forecast aligns with Morgan Stanley’s outlook, which anticipates strong U.S. economic growth and robust corporate earnings. Both firms expect the Federal Reserve to cut interest rates, further supporting business expansion.

Goldman highlighted the ‘Magnificent 7’—Amazon, Apple, Alphabet, Meta, Microsoft, Nvidia, and Tesla—as key drivers of growth, though their outperformance margin will narrow to the lowest level in seven years. The bank also foresees a potential 11% growth in corporate earnings and 2.5% real GDP growth by 2025, while cautioning about risks from higher bond yields and tariff policies under the newly re-elected Trump administration.

Investment Insight: Goldman’s outlook underscores the importance of balancing exposure between tech giants and broader market opportunities. Investors should be mindful of macroeconomic risks, including potential tariff impacts and bond yield fluctuations.

Market price: S&P 500: $5,893.62

Chinese Courier SF Holding Aims to Raise $793 Million in Hong Kong Listing

SF Holding, China’s largest express-delivery company, is looking to raise up to HK$6.2 billion ($793 million) through a Hong Kong listing, offering 170 million shares at HK$32.30 to HK$36.30 each. The share sale, expected to close on November 27, offers a roughly 29% discount to its Shenzhen-listed stock. SF Holding has already secured $205 million from cornerstone investors, including Xiaomi and Oaktree Capital.

Despite a slight recovery in Chinese investor sentiment after government stimulus measures, volatility persists amid ongoing U.S.-China trade tensions. Hong Kong IPOs have raised over $9 billion in 2024, yet the total remains below historical highs.

Investment Insight: SF Holding’s planned listing offers exposure to China’s logistics sector but comes with risks tied to trade tensions and market volatility. Investors should weigh the discounted pricing against the broader economic uncertainties.

Market price: S.F. Holding Co Ltd.: CNY 42.26

China Restricts Local Funds from Buying LGFV Bonds via Hong Kong Link

China has directed domestic investors to halt purchases of offshore yuan bonds issued by local government financing vehicles (LGFVs) through the Bond Connect program with Hong Kong, according to sources. The move comes as part of Beijing’s efforts to mitigate risks from the heavily indebted LGFV sector, which borrowed extensively during past infrastructure booms. This follows a recent $1.4 trillion debt swap initiative aimed at reducing “hidden” local government debt.

Local governments, hit by falling land sale revenues due to China’s property market crisis, are grappling with debt servicing challenges. LGFVs have been major issuers in the dim sum bond market, which has seen record issuance in 2024. The average coupon for LGFV dim sum bonds this year is 5.8%, significantly higher than their onshore equivalents.

Investment Insight: China’s tightening of restrictions on LGFV debt underscores the growing concerns about financial stability. Investors should be cautious of elevated yields in this sector, as further regulatory interventions may lead to increased volatility.

Delivery Hero Aims to Raise $1.5 Billion from Talabat’s Dubai IPO

Delivery Hero SE is targeting up to $1.5 billion through an IPO of its Middle Eastern unit, Talabat, in what could be one of 2024’s largest deals in the region. The company is offering a 15% stake, or 3.49 billion shares, at a price range of 1.50 to 1.60 dirhams each. The offering values Talabat at up to $10.2 billion, just below Delivery Hero’s $11 billion market cap. Major investors, including the UAE Strategic Investment Fund and Abu Dhabi Pension Fund, will contribute $250 million as cornerstone investors.

Investment Insight: Talabat’s IPO offers exposure to a high-growth, profitable food delivery platform in the Middle East. However, with recent IPOs in the region underperforming initially, investors should weigh the short-term market sentiment against long-term growth potential.

Conclusion:

In conclusion, the newsletter highlights a mix of optimism and caution in global markets. While Goldman Sachs and Morgan Stanley project strong U.S. economic growth, risks loom from potential tariff policies and bond yield fluctuations. In China, SF Holding’s IPO and restrictions on LGFV bond purchases underscore the complex interplay between market opportunities and regulatory challenges. Delivery Hero’s Talabat IPO offers a bright spot in the Middle East, while Asian markets remain sensitive to global trade tensions and China’s economic uncertainties. As investors navigate these dynamics, a balanced approach that considers both short-term sentiment and long-term potential is crucial.

Upcoming Dates to Watch:

- November 20, 2024: U.S. Federal Open Market Committee (FOMC) meeting minutes

- November 22, 2024: Japan National CPI release

- November 28, 2024: Eurozone Economic Sentiment Indicator release

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.

Daily Synopsis of the New York market close

Date Issued – 18th November 2024

Preview

Global markets experienced mixed performance as U.S. stocks slumped, with the S&P 500 and Nasdaq falling sharply due to concerns over President-elect Donald Trump’s policies. Asian shares saw varying results, with Japan’s Nikkei 225 dropping 1% while South Korea’s Kospi surged 2%. Indian bonds faced the largest outflows since their inclusion in JPMorgan’s emerging-market bond index, driven by rising U.S. Treasury yields. Samsung Electronics shares soared up to 7.5% following a surprise $7.2 billion buyback plan. Options traders are unwinding bullish bets on U.S. stocks amid concerns over slower interest rate cuts. Goldman Sachs predicts gold will hit a record $3,000 an ounce by December 2025, citing central bank buying and expected U.S. interest rate cuts. Investors are advised to consider defensive positions, diversify portfolios across global regions, and increase exposure to precious metals to hedge against potential risks.

Global Markets Struggle Amid U.S. Stock Slump

Asian shares kicked off the week with mixed results following Wall Street’s worst loss since Election Day. Japan’s Nikkei 225 dropped 1%, pressured by a stronger yen after Bank of Japan Governor Kazuo Ueda signaled continued interest rate hikes. South Korea’s Kospi surged 2%, driven by a 6% jump in Samsung Electronics after announcing a share buyback plan. Chinese markets also advanced, buoyed by retail data suggesting government stimulus is aiding economic recovery. Meanwhile, U.S. stocks saw sharp declines, with the S&P 500 down 1.3% and the Nasdaq falling 2.2%, as concerns over President-elect Donald Trump’s policy impact on vaccine manufacturers and biotech firms weighed on sentiment.

Investment Insight: Market volatility remains high, particularly in sectors sensitive to political developments. Investors should consider defensive positions and diversify portfolios across global regions to hedge against potential U.S. policy risks.

Market price: Nikkei 225: JPY 38,220.50

Indian Bonds Hit by Largest Outflows Since Index Inclusion

Foreign investors are pulling out of Indian bonds at the fastest rate since June, driven by rising U.S. Treasury yields that have reduced the relative appeal of Indian fixed-income securities. Data from the Clearing Corporation of India shows a net sale of 49.6 billion rupees ($588 million) of Fully Accessible Route bonds last week, marking the largest weekly outflow since their inclusion in JPMorgan’s emerging-market bond index. The shrinking yield gap between U.S. and Indian bonds, along with the Reserve Bank of India’s cautious stance on rate cuts, has further pressured Indian debt markets. However, upcoming index changes may mitigate the selloff, as JPMorgan plans to boost India’s bond weighting by the end of November.

Investment Insight: The narrowing yield spread between Indian and U.S. bonds signals a more challenging environment for Indian fixed-income assets. Investors should assess the impact of global interest rate trends and consider rotating into markets with more favorable yield differentials.

Market price: Nifty 50: INR 23,490.50

Economic Insights

Lenovo’s AI Momentum Drives Earnings and Outlook

Lenovo reported a strong earnings boost, with net profit for the September quarter rising 44% year-over-year to $359 million, surpassing analyst expectations. Revenue increased by 24% to $17.85 billion, driven by investments in AI and growth in PCs and smartphones. The company’s AI-enabled PCs have fueled a global market recovery, with the intelligent-devices segment showing a 17% revenue gain. Lenovo is diversifying beyond PCs, with non-PC revenue now comprising 46% of total sales. Despite robust growth in its infrastructure solutions, profitability remains a challenge due to low-margin projects aimed at capturing AI server market share.

Investment Insight: Lenovo’s focus on AI and diversification suggests potential for long-term growth. However, the path to profitability in emerging segments may be extended, requiring careful investor consideration.Market price: Lenovo Group Ltd. (0992.HK): HKD 9.17

New Alumina Supplies in 2025 Set to Curb Price Surge

New alumina capacity coming online in 2025 is expected to ease supply constraints and potentially end the record price rally. Alumina prices surged 70% this year due to supply disruptions in Guinea, Brazil, and Australia. However, new refineries in Indonesia, India, and China are set to boost production. China’s alumina exports rose 33% this year, and analysts predict a market surplus in 2025, leading to lower prices. UBS forecasts a drop to 3,600 yuan per ton, while Antaike estimates 4,000 yuan. A potential supply glut looms, especially if demand growth slows.

Investment Insight: Investors should prepare for potential price declines in alumina as new supply enters the market. Watch for shifts in demand and production rates that could impact profitability in the sector.Market price: Alumina: $411.16

Malaysia’s Economy Maintains Strong Growth Momentum in Q3 2024

Malaysia’s economy expanded by 5.3% year-on-year in the third quarter of 2024, driven by a surge in investments and increased domestic spending. The growth matched the advance estimate and Bloomberg’s median forecast. Sequentially, the economy grew by 1.8% from the previous quarter.

The Finance Ministry has raised its annual growth projection to 4.8%-5.3% for 2024 and expects further improvement in 2025. The central bank affirmed these revised forecasts, citing domestic spending as the main anchor for sustained growth, along with investments and improved exports.

Malaysia’s resilient economy is well-positioned to withstand potential pressure from financial market volatility following the US election. The central bank is liberalizing its foreign exchange policy to support investments, which is expected to spur the domestic bond and Islamic securities markets.

Investment Insight: Malaysia’s strong economic performance and the government’s proactive measures to attract investments make it an attractive destination for global investors. The country’s diversified economy and trade partnerships provide a stable foundation for growth, while the liberalization of foreign exchange policies further enhances its investment appeal. However, investors should monitor potential risks arising from geopolitical tensions and policy uncertainty following the US election.Market price: FTSE Bursa Malaysia KLCI: MYR 1,592.44

Conclusion:

Economic developments across Asia and beyond indicate both recovery and potential volatility. China’s growth initiatives, Lenovo’s AI-driven outlook, Japan’s anticipated rate hikes, and Malaysia’s policy measures highlight opportunities across diverse sectors. Additionally, alumina price adjustments provide new perspectives in commodities. Staying attuned to these changes will be essential for navigating complex market dynamics.

Upcoming Dates to Watch:

- November 20, 2024: U.S. Federal Open Market Committee (FOMC) meeting minutes

- November 22, 2024: Japan National CPI release

- November 28, 2024: Eurozone Economic Sentiment Indicator release

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.

Daily Synopsis of the New York market close

Date Issued – 15th November 2024

Preview

China’s economy showed signs of recovery in October, supported by growth-friendly policies, although the real estate sector continues to struggle. Lenovo reported strong earnings, driven by AI investments and growth in PCs and smartphones, but profitability in emerging segments remains a challenge. Japan’s economy grew modestly in Q3, and the central bank is expected to raise interest rates soon. New alumina capacity in 2025 is set to ease supply constraints and potentially end the record price rally. Malaysia’s economy maintained strong growth momentum in Q3 2024, driven by investments and domestic spending, with the government raising its annual growth projection and liberalizing foreign exchange policies to attract investments.

China’s Economy Shows Signs of Recovery Amid Stimulus Efforts

China’s economy displayed signs of improvement in October, supported by recent growth-friendly policies. Industrial production rose by 5.3% year-over-year, and retail sales grew by 4.8%, surpassing expectations. Despite these gains, the real estate sector continues to struggle, and concerns loom as Donald Trump’s re-election could lead to renewed trade tensions with the U.S. Economists suggest further measures, including fiscal stimulus, may be necessary to sustain growth.

Investment Insight: China’s short-term recovery is promising, but potential trade conflicts and a fragile real estate market pose risks. Investors should watch for further policy interventions to support sustained economic growth.

Market price: Shanghai Composite Index: CNY 3,330.73

Japan’s Economy Slows; Central Bank Likely to Raise Rates

Japan’s economy grew by 0.2% in the third quarter, supported by a 0.9% rise in private consumption due to summer bonuses and tax cuts. Despite slowing growth, the Bank of Japan is expected to raise interest rates soon, driven by improved consumer spending and a weaker yen. However, concerns remain about private-sector demand and potential deflation risks, especially with global uncertainties under President-elect Trump.

Investment Insight: Japan’s modest growth and expected rate hikes suggest cautious optimism. Investors should monitor consumer trends and global economic impacts on Japan’s recovery.

Market price: Nikkei 225: JPY 38,642.91

Economic Insights

Lenovo’s AI Momentum Drives Earnings and Outlook

Lenovo reported a strong earnings boost, with net profit for the September quarter rising 44% year-over-year to $359 million, surpassing analyst expectations. Revenue increased by 24% to $17.85 billion, driven by investments in AI and growth in PCs and smartphones. The company’s AI-enabled PCs have fueled a global market recovery, with the intelligent-devices segment showing a 17% revenue gain. Lenovo is diversifying beyond PCs, with non-PC revenue now comprising 46% of total sales. Despite robust growth in its infrastructure solutions, profitability remains a challenge due to low-margin projects aimed at capturing AI server market share.

Investment Insight: Lenovo’s focus on AI and diversification suggests potential for long-term growth. However, the path to profitability in emerging segments may be extended, requiring careful investor consideration.

Market price: Lenovo Group Ltd. (0992.HK): HKD 9.17

New Alumina Supplies in 2025 Set to Curb Price Surge

New alumina capacity coming online in 2025 is expected to ease supply constraints and potentially end the record price rally. Alumina prices surged 70% this year due to supply disruptions in Guinea, Brazil, and Australia. However, new refineries in Indonesia, India, and China are set to boost production. China’s alumina exports rose 33% this year, and analysts predict a market surplus in 2025, leading to lower prices. UBS forecasts a drop to 3,600 yuan per ton, while Antaike estimates 4,000 yuan. A potential supply glut looms, especially if demand growth slows.

Investment Insight: Investors should prepare for potential price declines in alumina as new supply enters the market. Watch for shifts in demand and production rates that could impact profitability in the sector.

Market price: Alumina: $411.16

Malaysia’s Economy Maintains Strong Growth Momentum in Q3 2024

Malaysia’s economy expanded by 5.3% year-on-year in the third quarter of 2024, driven by a surge in investments and increased domestic spending. The growth matched the advance estimate and Bloomberg’s median forecast. Sequentially, the economy grew by 1.8% from the previous quarter.

The Finance Ministry has raised its annual growth projection to 4.8%-5.3% for 2024 and expects further improvement in 2025. The central bank affirmed these revised forecasts, citing domestic spending as the main anchor for sustained growth, along with investments and improved exports.

Malaysia’s resilient economy is well-positioned to withstand potential pressure from financial market volatility following the US election. The central bank is liberalizing its foreign exchange policy to support investments, which is expected to spur the domestic bond and Islamic securities markets.

Investment Insight: Malaysia’s strong economic performance and the government’s proactive measures to attract investments make it an attractive destination for global investors. The country’s diversified economy and trade partnerships provide a stable foundation for growth, while the liberalization of foreign exchange policies further enhances its investment appeal. However, investors should monitor potential risks arising from geopolitical tensions and policy uncertainty following the US election.

Market price: FTSE Bursa Malaysia KLCI: MYR 1,592.44

Conclusion:

Economic developments across Asia and beyond indicate both recovery and potential volatility. China’s growth initiatives, Lenovo’s AI-driven outlook, Japan’s anticipated rate hikes, and Malaysia’s policy measures highlight opportunities across diverse sectors. Additionally, alumina price adjustments provide new perspectives in commodities. Staying attuned to these changes will be essential for navigating complex market dynamics.

Upcoming Dates to Watch:

- November 20, 2024: U.S. Federal Open Market Committee (FOMC) meeting minutes

- November 22, 2024: Japan National CPI release

- November 28, 2024: Eurozone Economic Sentiment Indicator release

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.

Daily Synopsis of the New York market close

Date Issued – 14th November 2024

Preview

Asia shares wobbled on Thursday amid concerns over China’s economic outlook and rising U.S. bond yields. Chinese property market woes weighed on regional indexes, while longer-term Treasury yields climbed on mixed inflation signals and expectations of Trump’s return to the White House.

In other news, Japan’s yen faces depreciation pressures despite a record current-account surplus, Nippon Steel’s VP seeks U.S. steelworker support for a takeover bid, Zeekr plans to acquire a controlling stake in Lynk & Co, and an IMF study highlights widening wealth gaps between Europe and the U.S. due to cross-border challenges. Geely Automobile nearly doubled its profit on strong sales, with its stock significantly outperforming the Hang Seng Index.

Asia Shares Wobble Amid China Concerns, U.S. Bond Yields Rise

Asian markets stumbled on Thursday, weighed down by weak Chinese stocks, as investors remain wary of the country’s economic outlook despite recent government support measures. Broader regional indexes followed suit, with Hong Kong’s Hang Seng Index dropping 0.34% and Japan’s Nikkei slipping 0.14%, as Chinese property market woes persist.

In the U.S., longer-term Treasury yields climbed, with the 10-year yield peaking at 4.483%, as markets digested mixed signals on inflation and the monetary policy impact of Donald Trump’s return to the White House. Meanwhile, Bitcoin held steady above $90,000, continuing its recent surge on optimism about the pro-crypto stance of the incoming administration.

Despite rising bets of a Federal Reserve rate cut in December, Trump’s plans for lower taxes and higher tariffs are expected to fuel inflation, limiting the Fed’s room to ease rates further in 2025.

Investment Insight: Investors should brace for increased volatility in global markets as U.S. fiscal policies under a Trump administration could push inflation higher, complicating the Federal Reserve’s path for rate cuts. In Asia, the ongoing struggles in China’s property sector remain a drag, potentially affecting regional growth.

Market price: Hang Seng Index: 19,435.81

Yen Weakens as Capital Outflows Overshadow Surplus

Japan’s yen continues to face depreciation pressures, driven by significant capital outflows despite a record current-account surplus of ¥8.97 trillion ($57.5 billion) in the third quarter. These outflows, particularly in direct and portfolio investments, are outpacing the surplus, limiting the yen’s potential gains. While Japan’s trade balance shows deficits, its primary income surplus—mostly investment returns—is reinvested abroad, further weakening the currency. With low domestic growth and limited foreign direct investment into Japan, the yen remains under strain, exacerbated by widening interest-rate differentials with the U.S.

Investment Insight: The yen’s persistent weakness signals limited domestic opportunities and increasing reliance on foreign investments. Investors should weigh the risks of currency depreciation against hedged holdings, especially with low growth prospects in Japan’s economy.

Market price: USD/JPY: 156.21

Market Updates

Nippon Steel’s VP to Meet U.S. Steelworkers Amid Takeover Uncertainty

Nippon Steel Corp.’s Vice President Takahiro Mori will meet with union representatives from U.S. Steel’s Pittsburgh plants next week, aiming to garner worker support for the company’s $14.1 billion takeover bid. Although President-elect Donald Trump has vowed to block the deal, Mori’s outreach signals an attempt to sway rank-and-file steelworkers, many of whom have shown support for the acquisition. The deal remains under review by the Committee on Foreign Investment in the U.S. (CFIUS), and a final decision is expected by December.

Investment Insight: The pending takeover of U.S. Steel by Nippon Steel could face headwinds from political opposition, but worker support may help push the deal forward. Investors should monitor regulatory decisions and union negotiations closely, as these factors will likely influence the deal’s outcome and future market dynamics in the steel industry.

Market price: Nippon Steel Corp. (5401.T): JPY 3,067.00

Zeekr to Take Control of Sister Brand Lynk in Strategic Move

Chinese electric vehicle maker Zeekr is set to acquire a controlling stake in Lynk & Co, a sister brand co-owned by Geely and Volvo Cars. According to sources, the deal will involve Zeekr purchasing Volvo’s 30% stake and a 20% stake from Geely Holding, valuing Lynk & Co at approximately 18 billion yuan ($2.5 billion). This move is part of Geely’s broader strategy to streamline operations and cut costs. The transaction will increase Zeekr’s stake to 51%, with finalization expected by June 2025.

Investment Insight: This consolidation effort by Geely could enhance operational efficiency and strengthen Zeekr’s position in the competitive EV market. Investors should monitor how this restructuring affects financial performance and market share, particularly in the fast-growing premium electric vehicle segment.

Market price: Volvocar (VOLCAR-B.ST): SEK 24.13

IMF Study: Cross-Border Challenges Widen Wealth Gap Between Europe and U.S.

A new IMF study reveals that cross-border challenges are widening the wealth gap between Europe and the U.S., with the EU’s GDP per capita now at just 72% of the U.S. level. The report attributes 70% of this gap to slower productivity growth in Europe, largely due to trade barriers between EU nations, which hinder firms from fully leveraging the bloc’s large market. Additionally, fragmented capital markets and limited labor mobility in Europe further constrain productivity. The IMF suggests that lowering trade barriers and improving capital flows could significantly boost European productivity.

Investment Insight: Investors should note the structural challenges facing European markets, particularly in sectors reliant on cross-border efficiency and capital. The slow progress on removing these barriers may continue to hamper Europe’s competitiveness, especially against the more unified U.S. market.

Market Price: Euro Stoxx 50 Index: EUR 4,798.34

Geely Automobile Nearly Doubles Profit on Strong Sales

Geely Automobile posted an impressive 92% surge in third-quarter net profit, reaching 2.46 billion yuan ($340.5 million), with revenue up 20% to 60.38 billion yuan. The Chinese automaker credited robust sales at home and abroad, along with a diversified product mix featuring brands like Zeekr and Lynk & Co., for its stellar performance. Geely’s stock has soared 64% this year, significantly outperforming the Hang Seng Index. The China Passenger Car Association expects continued strong demand for Chinese electric vehicles through year-end, fueled by government incentives and competitive market conditions.

Investment Insight: Geely’s robust financial performance, driven by its diverse vehicle lineup and expanding EV presence, signals growth potential for investors. With government support for EVs and strong market momentum, Geely’s stock may continue to outperform, especially as it capitalizes on the global shift toward clean energy transportation.

Market Price: Geely Automobile Holdings Ltd.: HKD 13.90

Conclusion

With U.S. fiscal policy changes and inflationary pressures, Asian markets are experiencing increased volatility. In Japan, the yen’s depreciation is a key issue for investors, while in the steel industry, regulatory approval remains critical for Nippon Steel’s takeover bid. Geely’s impressive earnings and strategic EV moves highlight growth potential in China’s auto market, while the IMF’s findings on Europe’s productivity underscore structural issues that may affect investment opportunities.

Upcoming Dates to Watch:

- November 15, 2024: Eurozone Q3 GDP report release

- November 20, 2024: U.S. Federal Open Market Committee (FOMC) meeting minutes

- November 22, 2024: Japan National CPI release

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.

Daily Synopsis of the New York market close

Date Issued – 13th November 2024

Preview

CATL, the world’s largest battery maker, is expanding into green energy grids and EV platforms, eyeing opportunities in the U.S. market. Swiggy’s successful IPO defies India’s weak market, signaling resilience in the quick-commerce sector. Japan’s Seven & i explores a $58 billion management buyout to resist a takeover by Canada’s Couche-Tard. President-elect Trump taps Elon Musk and Vivek Ramaswamy to lead a new “Department of Government Efficiency” initiative. Yen-hedged U.S. Treasury yields are set to turn positive for the first time in two years, potentially renewing Japanese investor interest.

CATL Expands Beyond Batteries Into Green Energy and EV Platforms, Eyes U.S. Market

Chinese battery giant CATL, the world’s largest, is making bold moves to expand beyond its core EV battery business. Founder Robin Zeng is pushing CATL into two new areas: developing zero-carbon electric grids and offering off-the-shelf EV platforms. The energy grid business, which leverages renewable sources like solar and wind, could become ten times larger than CATL’s current battery segment, according to Zeng, challenging the dominance of China’s state oil giants. Meanwhile, CATL’s EV platform integrates long-range batteries directly into the chassis, aiming to slash EV development costs and open the market to new players.

While these ventures represent a significant strategic shift, CATL is also open to building a U.S. plant if President-elect Donald Trump reduces trade barriers. Though U.S.-China tensions have previously stifled Chinese investments in the EV supply chain, Zeng remains optimistic about future opportunities. The company already licenses its battery technology to U.S. giants like Tesla and Ford, and further expansion could depend on shifting political winds.

Investment Insight

CATL’s aggressive push into green energy grids and cost-efficient EV platforms offers substantial growth potential, positioning it as a leader in the clean energy transition. Investors should track the company’s ability to scale these new initiatives while navigating geopolitical complexities, particularly with its potential U.S. expansion hinging on trade policy changes.

Market price: CATL (300750.SZ): 282.00 CNY

Swiggy’s India IPO Defies Market Weakness with Strong Debut

Swiggy Ltd. made a successful stock market debut in Mumbai, with shares rising over 7% from the IPO price of 390 rupees to 420.05 rupees. The $1.3 billion IPO, India’s second-largest this year, overcame initial lukewarm demand, bolstered by strong institutional interest on the final day. Swiggy’s listing comes amid a competitive quick-commerce landscape dominated by larger rival Zomato and privately-held Zepto. Despite facing regulatory scrutiny and operating at a loss, Swiggy’s growth trajectory is supported by India’s booming online retail market, which analysts predict will expand significantly over the next decade.

Investment Insight

Swiggy’s IPO performance signals resilience in India’s quick-commerce sector despite a weak market for large listings. Investors should monitor competitive dynamics and regulatory risks, but Swiggy’s growth potential in a $1 trillion retail market makes it a promising long-term play.

Market price: Swiggy Ltd (Mumbai): 446.95 INR

Seven & I Explores $58 Billion Management Buyout Amid Takeover Threat

Seven & i Holdings, the operator of 7-Eleven stores, is exploring a management buyout worth around ¥9 trillion ($58 billion) to resist a potential takeover by Canadian convenience store giant Alimentation Couche-Tard. The buyout, backed by Japan’s top megabanks and trading house Itochu Corp., would be the largest-ever in Japan. The move is seen as a defensive strategy to keep the company, which has been restructuring, under domestic control. Couche-Tard had previously increased its offer for Seven & i to ¥7.2 trillion, marking the largest-ever foreign takeover attempt of a Japanese company.

Investment Insight

The potential management buyout of Seven & i reflects Japan’s deep resistance to foreign takeovers, a rare event in the country’s corporate landscape. Investors should watch for further developments in the buyout talks, as they could offer significant implications for corporate Japan and the global retail sector.

Market price: Seven & i Holdings (3382.T): 2,490.00 JPY

Trump Taps Musk, Ramaswamy to Lead “Department of Government Efficiency”

President-elect Donald Trump announced that Elon Musk and former GOP candidate Vivek Ramaswamy will spearhead a new initiative dubbed the “Department of Government Efficiency” (DOGE), aimed at streamlining federal operations. Though not an official government agency, the group will work externally with the White House and the Office of Management and Budget to drive cost-cutting reforms. Musk, a frequent visitor to Mar-a-Lago, has previously claimed he could identify $2 trillion in government savings. The group, operating outside traditional federal regulations, will not be bound by typical conflict of interest or disclosure rules.

Investment Insight

Musk’s role in advising on government efficiency may strengthen his influence in Washington, potentially impacting sectors like energy, aerospace, and technology. Investors should monitor how his recommendations could reshape federal spending and regulatory policies, which could have ripple effects across multiple industries.

Market price: Tesla (TSLA): $328.49

Treasury Yields Set to Turn Positive for Yen-Hedged Investors

For the first time in two years, yen-hedged U.S. Treasury yields are poised to turn positive, driven by rising U.S. interest rates following Donald Trump’s election and easing hedging costs due to Federal Reserve rate cuts. The yield on 10-year Treasuries, adjusted for currency hedging, reached minus 13 basis points on Tuesday, after being negative since September 2022. While Japanese investors have been net sellers of Treasuries this year, the reduction in hedging costs could renew interest, particularly in higher-yielding U.S. agency and corporate bonds.

Investment Insight

As hedging costs decline, U.S. Treasuries may become more attractive for Japanese investors. However, with Japanese government bonds offering competitive returns, the pace of investment may depend on further shifts in U.S. yields and currency risks.

Market price: 10-Year U.S. Treasury Yield: 4.31%

Conclusion:

CATL’s expansion into renewable grids and EV platforms underscores China’s ambition in green energy, while Swiggy’s IPO signals resilience in India’s growing quick-commerce sector. In Japan, the potential buyout of Seven & i by domestic management reveals a strong stance against foreign takeovers. Meanwhile, President-elect Trump’s appointment of Musk and Ramaswamy to lead the “Department of Government Efficiency” could drive cost-cutting measures affecting sectors reliant on federal spending. Additionally, with U.S. Treasury yields becoming more attractive to yen-hedged investors, Japanese demand may see renewed interest.

Upcoming Dates to Watch:

- November 13, 2024: U.S. Consumer Price Index (CPI) data release

- November 14, 2024: Eurozone Q3 GDP report release

- November 20, 2024: U.S. Federal Open Market Committee (FOMC) meeting minutes

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.

Daily Synopsis of the New York market close

Date Issued – 12th November 2024

Preview

Baidu reveals new AI products, including text-to-image generator and no-code app tool, as it expands AI offerings. China’s surging copper production threatens global smelters, raising concerns over margins and overcapacity. Japan’s minority government could boost retail, utilities, and tech sectors, while investing heavily in semiconductors and AI. Oil prices remain weak due to demand concerns and strong dollar, as markets await OPEC guidance. Ivanhoe’s Friedland downplays US tariff impact on China, citing reduced export reliance. Asian stocks retreat while Bitcoin soars on Trump euphoria, with investors betting on pro-growth policies.

Baidu Expands AI Offerings with Text-to-Image and No-Code App Tools

Baidu Inc., China’s leading search engine, revealed new AI-driven products at its annual Baidu World Conference, signaling its push into large language model (LLM) applications. Among the highlights are I-RAG, a text-to-image generator designed to mitigate “hallucination” issues—common in AI image generation—and Miaoda, a tool that enables users to create software without needing coding skills. CEO Robin Li also noted that Baidu’s Ernie platform now handles 1.5 billion daily interactions, up from 200 million in May, underscoring the company’s rapid AI expansion. Additionally, Baidu debuted AI-powered smart glasses, further integrating AI into its product ecosystem.

Investment Insight

Baidu’s strategic focus on AI commercialization, particularly through scalable tools like no-code solutions and smart hardware, positions it as a key player in China’s AI race. Investors should monitor Baidu’s ability to convert these innovations into revenue streams amidst competition from domestic rivals like ByteDance.

Market price: Baidu Inc. (BIDU): $88.20

China’s Copper Production Surge Threatens Global Smelters

China’s rapid expansion in copper production is squeezing margins globally and could force smelters in countries like Chile and Europe to scale back. As China approaches 50% of the world’s refined copper output, its smelters continue to grow capacity despite shrinking treatment fees, increasing pressure on global operations. With demand for copper set to soar—driven by the energy transition and electric vehicles—China’s dominance in refining capacity is raising concerns internationally. This week’s Asia Copper Week in Shanghai will see key industry players discuss the worsening ore supply gap and potential curtailments outside China.

Meanwhile, Russia’s MMC Norilsk Nickel is exploring plans to build a 500,000-ton copper smelter in southern China, further strengthening China’s grip on copper processing.

Investment Insight

China’s copper production boom creates headwinds for non-Chinese smelters, with growing overcapacity and margin compression as key risks. Investors should keep a close eye on China’s ability to manage overproduction while maintaining profitability in the face of global demand shifts.

Market price: Copper Futures: $4.188 per pound

Weak Government in Japan Could Boost Retail, Utilities, and Tech, While Semiconductors Get Major Support

Japan’s minority government under Prime Minister Shigeru Ishiba may provide a boost to sectors like retail, utilities, and tech, as the administration looks to maintain support from opposition parties. Tax cuts aimed at increasing disposable income are on the table, which could benefit consumer-facing companies such as Ryohin Keikaku and Shimamura if the Democratic Party for the People (DPP) succeeds in raising the tax-free income ceiling. At the same time, the opposition’s pro-nuclear stance is likely to support utility stocks, as plans to restart additional reactors move forward.

Meanwhile, Ishiba has also announced a massive ¥10 trillion ($65 billion) investment in Japan’s semiconductor and AI sectors, aiming to unlock ¥50 trillion in public and private investment over the next decade. This initiative is part of a broader effort to ensure Japan remains competitive in the global chip race, particularly as the U.S. and China pour resources into advanced semiconductor technologies. The funding is expected to drive growth in Japan’s tech sector, with companies like Renesas Electronics and Tokyo Electron well-positioned to benefit from the government’s AI and chip ambitions.

Investment Insight

Retail and utility stocks stand to gain from increased disposable income and pro-nuclear policies, while tech firms could see long-term growth from Japan’s aggressive investment in AI and semiconductors. However, political gridlock may slow decision-making on military spending and corporate reforms, creating challenges for defense-related stocks. Investors should focus on the opportunities in Japan’s chip sector as public and private investment accelerates under favorable policy frameworks.

Market price: Nikkei 225: JPY 39,376.09

Oil Holds Biggest Drop in Two Weeks Amid Demand Concerns and Strong Dollar

Oil prices remained weak after the largest drop in two weeks, driven by concerns over soft demand in China, a stronger US dollar, and fears of a potential oversupply. Brent crude traded below $72 following a 3% decline, while West Texas Intermediate hovered around $68. China’s latest economic measures have failed to provide direct stimulus, and weak inflation adds to the uncertainty. Meanwhile, the dollar’s strength, fueled by Donald Trump’s election victory, has made oil more expensive for non-US buyers. With global supply expected to exceed demand in 2025, markets are closely watching OPEC’s monthly report for further guidance.

Investment Insight

Oil markets face bearish sentiment due to US dollar strength, weak demand forecasts, and oversupply concerns. Investors should monitor OPEC+ decisions and potential US sanctions enforcement against Iran as key factors that could shift the outlook for crude prices in 2025.

Market price:

Brent Crude: $71.90 per barrel

WTI Crude: $68.06 per barrel

Ivanhoe’s Friedland Downplays US Tariff Impact on China

Robert Friedland, founder of Ivanhoe Mines Ltd., believes China is better positioned to withstand US tariffs under Donald Trump’s incoming administration due to its reduced reliance on exports to the US. In an interview, Friedland noted that China’s economic exposure to the US has significantly decreased since Trump’s first term, making it less vulnerable to the president-elect’s proposed 60% tariffs. He also highlighted China’s ongoing efforts to stimulate domestic demand and address local government debt, asserting that China’s long-term outlook remains strong. Friedland expressed optimism about the US as well, citing Trump’s alignment with technology leaders like Elon Musk as a potential boost for innovation.

Investment Insight

China’s reduced dependence on US exports mitigates immediate risks from new tariffs, offering resilience to its economy. Investors might find opportunities in Chinese equities, which are attractively priced compared to US stocks, while keeping an eye on potential trade negotiations between the two superpowers.

Market Price: Ivanhoe Mines (IVN.TO): CAD 18.33

Asian Stocks Retreat, Bitcoin Soars on Trump Euphoria

Asian stocks slid on Tuesday, with Taiwan and South Korea leading the declines, while the dollar held at four-month highs. Markets are reacting to Donald Trump’s re-election, with investors betting on pro-growth policies like tax cuts and deregulation. Bitcoin surged to an all-time high of $89,637, buoyed by expectations of a favorable regulatory environment for cryptocurrencies under Trump’s second term. Meanwhile, the euro weakened to near seven-month lows due to concerns over potential tariffs from the new White House administration.

In Japan, the Nikkei gained 0.5% on a weaker yen, bucking the regional trend. U.S. chip restrictions on China have hurt stocks like Taiwan Semiconductor, adding pressure in the tech sector. Wall Street hit record highs overnight, with Tesla jumping 9% on optimism surrounding Trump and Elon Musk’s continued leadership.

Investment Insight

Investors are riding a wave of optimism on Trump’s re-election, with bitcoin and equities seeing strong gains. However, risks remain, particularly around potential tariffs and inflationary pressures. Watch for volatility as markets digest the full implications of Trump’s policies, especially in tech and trade-sensitive sectors.

Market price: Bitcoin (BTC): $89,702.32

Conclusion:

The market landscape is evolving as Trump’s re-election prompts reactions across various sectors, from energy and technology to Asian and U.S. markets. As these changes unfold, our aim is to provide insights to guide your investment decisions. We are here to discuss strategies and portfolio adjustments in light of these complex developments.

Upcoming Dates to Watch:

- November 13, 2024: U.S. Consumer Price Index (CPI) data release

- November 14, 2024: Eurozone Q3 GDP report release

- November 20, 2024: U.S. Federal Open Market Committee (FOMC) meeting minutes

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.