Date Issued – 26th November 2024

Preview

Asian markets slipped on Tuesday amid concerns over potential tariffs on Mexico, Canada, and China, as mentioned by President-elect Donald Trump.

The Nikkei 225, S&P/ASX 200, and Kospi declined, while the Hang Seng remained flat. China is ramping up Brazilian soybean imports due to trade tensions

with the U.S. and favorable prices. Qualcomm has cooled on its potential acquisition of Intel, citing financial and regulatory challenges.

Xiaomi is developing its own mobile processor to reduce dependence on Qualcomm and MediaTek, aligning with Beijing’s push for self-reliance in technology.

Best Buy is eyeing AI products for growth and expects to report flat Q3 earnings, with AI-enabled devices potentially offsetting sluggish appliance sales.

Asian Markets Slip Amid Tariff Concerns

Asian shares mostly fell on Tuesday following President-elect Donald Trump’s comments on imposing tariffs on Mexico, Canada, and China.

Japan’s Nikkei 225 dropped 0.9%, Australia’s S&P/ASX 200 slid 0.7%, and South Korea’s Kospi declined 0.6%. Meanwhile, Hong Kong’s Hang Seng was flat,

and the Shanghai Composite edged up 0.1%. Concerns over trade policy overshadowed Wall Street’s gains on Monday, where the S&P 500 rose 0.3%,

and the Dow hit a record high. U.S. Treasury yields eased after Trump floated hedge fund manager Scott Bessent as a potential Treasury Secretary,

fueling hopes of deficit control.

Investment Insight: Heightened trade tensions could weigh on Asian markets while lower U.S. Treasury yields may benefit equities.

Investors should monitor inflation data and Fed rate policy for near-term market direction.

China Ramps Up Brazilian Soybean Imports Amid Trade Tensions

Chinese buyers are securing record volumes of Brazilian soybeans, taking advantage of low prices and abundant supply from Brazil’s expected largest-ever harvest.

Concerns over renewed trade tensions with the U.S., as President-elect Donald Trump threatens new tariffs on Chinese goods, have pushed Chinese crushers to stock up early,

even during Brazil’s off-season. Brazilian soybeans are priced $22 per ton cheaper than U.S. beans for March deliveries, according to Commodity3 data.

While the U.S. still accounts for some Chinese purchases, sales remain at their lowest for this time of year since 2018, reflecting uncertainty over trade policies.

Investment Insight: China’s pivot to Brazilian soybeans signals potential headwinds for U.S. agriculture. Investors in commodities and agribusiness should

watch for tariff developments and shifts in global supply chains.

Qualcomm Cools on Intel Takeover Amid Complexities

Qualcomm has reportedly backed away from pursuing an acquisition of Intel, citing the deal’s financial and regulatory challenges, including Intel’s $50 billion debt and its

loss-making manufacturing unit. The potential takeover, which could have been one of the largest tech deals ever, faced antitrust hurdles and operational risks. Qualcomm may

still explore acquiring parts of Intel or revisit the idea in the future. Both firms are navigating shifting industry dynamics, with Qualcomm targeting new markets and Intel

striving to regain its footing in the AI-driven chip race.

Investment Insight: The cooled takeover reflects the growing complexity of mega-deals in the semiconductor sector. Investors should focus on Qualcomm’s organic

growth initiatives and Intel’s restructuring efforts for long-term opportunities.

Market price: QCOM: USD 158.82

Xiaomi Prepares In-House Chip, Targeting Qualcomm and MediaTek

Xiaomi is developing its own mobile processor, with mass production slated for 2025, aiming to reduce dependence on Qualcomm and MediaTek. This move aligns with Beijing’s

push for self-reliance in technology amid U.S.-China tensions. While Apple and Google have succeeded in designing proprietary chips, other firms like Oppo and Nvidia have

struggled, highlighting the challenges Xiaomi faces. In-house chipmaking could boost Xiaomi’s smartphone competitiveness and support its broader ambitions in connected tech,

including electric vehicles, as the company ramps up R&D investments to $4.1 billion in 2025.

Investment Insight: Xiaomi’s chip strategy could disrupt the supply chain dynamics for Qualcomm and MediaTek. Investors should watch for advancements in Xiaomi’s

semiconductor capabilities and its potential to reshape the Android device market.

Market price: Xiaomi: HKD 27.25

Best Buy Eyes AI Products for Growth Amid Stabilizing Demand

Best Buy is set to report its Q3 results, with Wall Street expecting flat adjusted earnings of $1.29 per share on $9.63 billion in revenue, slightly below last year. Same-store

sales are forecasted to dip nearly 1%, an improvement from a 7.3% decline a year ago. Appliance sales are expected to drag, while computing and mobile phones may see gains,

supported by demand for AI-enabled products like Copilot+ PCs. Best Buy remains optimistic about AI as a growth driver, with exclusivity deals on 40% of new AI PCs and a broader

rollout anticipated in 2025.

Investment Insight: Best Buy’s focus on AI products positions it to capitalize on tech-driven consumer trends. Investors should monitor its ability to offset

sluggish appliance sales with demand for emerging AI-enabled devices.

Market price: Best Buy Co (BBY): USD 93.03

Conclusion

The newsletter highlights the complex interplay of geopolitical tensions, technological advancements, and shifting consumer trends in shaping the global market landscape. As

trade tensions persist, companies are navigating supply chain disruptions and exploring new strategies for growth. The semiconductor industry faces challenges in mega-deals,

while the rise of AI presents opportunities for firms to differentiate and capture emerging demand. Investors should closely monitor these developments, focusing on companies’

ability to adapt and innovate in an increasingly dynamic and competitive environment. By staying attuned to these key trends, investors can position themselves to capitalize on

the long-term opportunities that arise.

Upcoming Dates to Watch:

November 28, 2024: Eurozone Economic Sentiment Indicator release

Bond Market Stabilizes as Bessent’s Treasury Nomination Calms Markets

The U.S. bond market is finding its footing after a two-month selloff, with investors stepping in at 4.5% yields.

Treasury yields, which peaked on Nov. 15, have since dipped to 4.36% following Scott Bessent’s nomination as U.S. Treasury Secretary.

Bessent, a fiscal hawk, has pledged to cut the deficit to 3% of GDP through spending cuts and economic growth, though skeptics question

the feasibility of reducing essential expenditures like Medicare and defense. His commitment to a strong dollar contrasts with Trump’s

past devaluation rhetoric, and his fiscally disciplined stance has eased market concerns, driving a 6-basis-point drop in 10-year yields.

Despite the recent rally, uncertainty over Trump’s fiscal policies, inflation, and potential tariffs—some as high as 60% on Chinese goods—keeps

volatility elevated. While some strategists see 4.25%-4.5% as fair value for 10-year Treasuries, others caution that yields could rise further

if aggressive fiscal stimulus boosts inflation. Traders are now awaiting the Fed’s preferred inflation gauge, the PCE price index, for additional clarity.

Investment Insight: Treasuries at 4.5% yields present attractive returns, but volatility may persist amid fiscal policy uncertainty.

Bessent’s nomination signals fiscal discipline, which could support bonds but pose risks for equities if aggressive deficit reduction slows growth.

Investors should monitor tariff developments, Fed-ECB rate divergence, and inflation data for guidance.

US10Y Yield: 4.328%

Meituan, Chow Tai Fook Earnings to Gauge China’s Consumer Sentiment

Earnings from Meituan and Chow Tai Fook Jewellery this week are set to provide insights into China’s struggling consumer market, weighed down

by a sluggish economic recovery, property woes, and job instability. Despite these headwinds, October retail sales saw their fastest growth in

eight months, supported by government stimulus efforts that have yet to meaningfully boost household incomes.

Meituan is expected to defy the broader slowdown, with Morgan Stanley predicting strong growth driven by consumption voucher programs and

policy support for platform economies. In contrast, Chow Tai Fook’s first-half earnings are likely to reflect weak retail sentiment and high gold prices,

with revenue projected to decline up to 22%.

Investment Insight: Meituan’s resilience highlights opportunities in platform-driven sectors benefiting from policy tailwinds,

while Chow Tai Fook underscores challenges in discretionary spending. Cautious positioning in China’s consumer sector is warranted until income growth stabilizes.

Market price: Meituan (3690.hk): HKD 161.00

Rio Tinto-Backed Lithium Startup Nears $19M Fundraising Amid Market Struggles

ElectraLith, a Rio Tinto-backed lithium technology startup, is set to close an oversubscribed A$29 million ($19 million) funding round despite weak global lithium

and venture capital markets. The company’s innovative direct lithium extraction (DLE) technology uses no water or chemicals, making it ideal for arid regions like

Chile’s Atacama Desert. ElectraLith plans to use the funds to construct its first pilot plant at Rio Tinto’s Rincon operations in Argentina within a year, followed

by two additional pilot plants. The DLE-R process, which filters brine to produce lithium hydroxide at half the cost of competitors, could revolutionize the lithium

industry by drastically shortening production timelines and addressing water scarcity challenges.

Investment Insight: ElectraLith’s cost-efficient and sustainable DLE technology positions it favorably in the growing lithium market,

which could surpass $10 billion annually within a decade. Investors should watch how the startup scales its technology and competes in the evolving EV battery supply chain.

Market Price: Rio Tinto: USD 62.50

Conclusion:

The global investment landscape is rapidly evolving, shaped by geopolitical shifts, technological innovation, and changing consumer trends.

As the U.S. navigates a political transition and China faces structural challenges, Southeast Asia grapples with the potential fallout from

Trump’s protectionist policies. Investors must remain vigilant, monitoring developments in key sectors like cryptocurrencies, bonds, consumer

goods, lithium, semiconductors, and EVs. Diversification and adaptability will be crucial in mitigating risks and seizing opportunities amidst

uncertainty. The coming weeks will provide further clarity on the future of these critical industries and the economies they support, as the world

braces for a new era of change.

Upcoming Dates to Watch:

November 28, 2024: Eurozone Economic Sentiment Indicator release

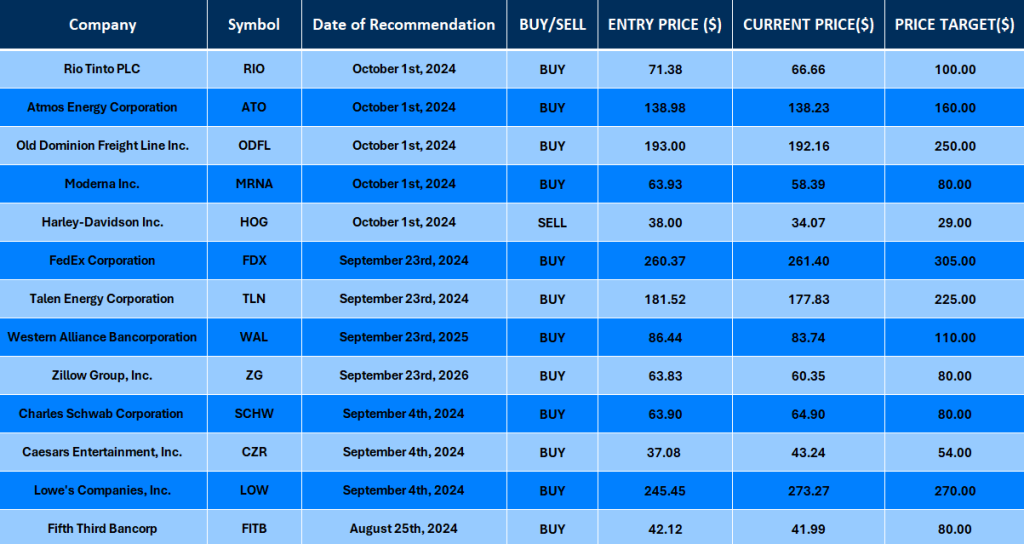

Find below some of our Buy/Sell Recommendations. Balfour Capital Group is a distinguished global boutique investment management firm with $400 million AUM and over 1000 Clients.

Disclaimer: This post provides financial insights for informational purposes only. It does not constitute financial advice or recommendations for investment decisions.